Phillip “Friends Can Agree to Disagree” Dampier

Are we being unnecessarily pessimistic and cynical when we oppose the likely nomination of Thomas Wheeler to replace Julius Genachowski as the chairman of the Federal Communications Commission?

Some of our colleagues in the consumer-focused public policy arena suspect we might be.

Stop the Cap! is very skeptical that appointing a former cable and wireless industry lobbyist with 30+ years of experience is the best choice for consumers at the FCC.

Our friend Harold Feld from Public Knowledge, which has announced cautious support for Wheeler’s appointment, has a more optimistic view about his potential:

I understand where my friends are coming from when they look at Wheeler’s resume and think “oh God, another Washington insider, why can’t we ever get a real progressive!” But I cannot agree with Senator Rockefeller’s statement that “a lobbyist, is a lobbyist,” or the view of some that the taint of industry clings insidiously forever and corrodes the soul. It’s been ten years since Wheeler left CTIA, longer than that since he left NTCA. Had he really been interested in advancing the agendas of these industries, he was in an excellent position to do so when he headed up the Obama transition team. He did not. Indeed, Susan Crawford and Kevin Werbach, long-time stalwarts of the public interest who worked for Wheeler on the transition team, have joined other public interest luminaries as Wheelers strongest public supporters. Had Wheeler been working behind the scenes in the transition to promote the incumbents, I expect Susan and Kevin would have known.

I also recognize that support from public interest friends is also not conclusive. But it should surely weigh in the evaluation of Wheeler as much as any blog post. And I recognize I’m also a “Washington insider” and as likely to be led astray by my personal friendships and the whole “Washington Bubble” culture as any other human being. That’s why I’m glad people in the community are asking the right questions and putting Wheeler on notice that, like any Chairman, he needs to prove himself as a champion of the public interest. We at PK have also made it clear we expect Wheeler to not just talk a good game, but to get his hands dirty and make tough decisions that will piss off incumbents. And when we disagree, as we expect we will, have no doubt we will make our displeasure known.

Harold specifically commented on our piece reviewing Wheeler’s personal blog, in which Wheeler fell all over himself praising AT&T’s chief lobbyist Jim Cicconi, and seemed resigned to approving a proposed AT&T/T-Mobile merger with some preconditions:

It is certainly true that behavioral conditions often fall short, are short lived, and that companies generally find ways to work around them (and the FCC’s track record for enforcement is pathetic). Indeed, we at PK made these arguments in the context of the AT&T/T-Mobile merger for why no set of merger remedies could adequately address the harms such a merger would cause. But there is a huge difference between my belief that Wheeler was wrong about the best strategy to advance the public interest and accepting that he was motivated by a covert desire to support consolidation and deregulation.

It is more than likely we will have to do business with Tom Wheeler, and we can certainly understand efforts to paint a more optimistic and hopeful picture of the likely new chairman. But we would be dishonest if we said we have high hopes Wheeler will think first about ordinary Americans before steering the country’s telecommunications future. We have learned from the past.

Remember Your History: Catering to Big Special Interests is Bipartisan

Having covered the telecommunications industry since the 1980s when Dr. John Malone of Tele-Communications, Inc., was the American consumers’ worst nightmare, confronting today’s increasingly consolidated and expensive telecommunications marketplace is a case of “Back to the Future.” The deregulation and industry consolidation abuses in the 1980s riled up both Republicans and Democrats — wherever constituents flooded offices with complaints about the local cable monopoly. The “problem politicians” that reflexively defended the abusers were just as bipartisan. Sen. Tim Wirth (D-Colo.) primarily represented the interests of the cable companies that were headquartered in his state. Current Senate Majority Leader Harry Reid (D-Nev.) also defended the cable companies. Sen. John Danforth (R-Mo.) was outraged at the abuses cable operators like TCI heaped on Missouri consumers and not only introduced legislation to stop the abuse in 1992, he also was instrumental in overriding a presidential veto of the measure.

Having covered the telecommunications industry since the 1980s when Dr. John Malone of Tele-Communications, Inc., was the American consumers’ worst nightmare, confronting today’s increasingly consolidated and expensive telecommunications marketplace is a case of “Back to the Future.” The deregulation and industry consolidation abuses in the 1980s riled up both Republicans and Democrats — wherever constituents flooded offices with complaints about the local cable monopoly. The “problem politicians” that reflexively defended the abusers were just as bipartisan. Sen. Tim Wirth (D-Colo.) primarily represented the interests of the cable companies that were headquartered in his state. Current Senate Majority Leader Harry Reid (D-Nev.) also defended the cable companies. Sen. John Danforth (R-Mo.) was outraged at the abuses cable operators like TCI heaped on Missouri consumers and not only introduced legislation to stop the abuse in 1992, he also was instrumental in overriding a presidential veto of the measure.

The first mistake one can make in this fight is characterizing this as “progressive” vs. “conservative.” Real conservatives want all-out competition to manage winners and losers. Progressives want to make sure in the absence of that competition, someone — anyone can act to check the power of concentrated markets that suppress competition, raise prices, and deliver less than compelling service. Five years ago, Barack Obama promised change and a D.C. reset that would have ended “politics as usual.”

The art of the possible — changing the perception that consumer interests take a back seat to the whims of professional lobbyists at the FCC has proved less than successful after four years with Julius Genachowski. President Obama is not completely responsible, but it would be dishonest not to hold him to a promise he would deliver “change we can believe in.”

Instead, at the FCC, we got “change we think we might be able to get away with, maybe, or not.”

Julius Genachowski remained silent on the AT&T/T-Mobile merger until the Department of Justice provided him with political cover to oppose it. He caved on strongly enforcing Net Neutrality, refused to make important regulatory declarations that would have satisfied federal courts the FCC has a right to oversee broadband policy, and near the end of his tenure, hobnobbed with the cable industry and declared his support for usage billing and capped Internet.

Where Does Mr. Wheeler Stand?

(Image: MuniNetworks)

So we must ask ourselves, where does Mr. Wheeler, a man who spent most of his career as a consummate cable and wireless industry lobbyist, fall on these issues?

The best place those of us who have not shared lunch with him can make that determination is in his personal blog. Harold wants us to downplay some of Wheeler’s words written during his six years of blogging:

But in the ten years I’ve been blogging, I know that I’ve said many things that do not necessary reflect what I would have done if I had been the ultimate decisionmaker – as I have said on more than one occasion (noting that actual decisionmakers are not advocates). Certainly anyone who reads ten years worth of Tales of the Sausage Factory (has it really been ten years?) will have an excellent sense of my overall priorities and approach. But I can’t swear that all approximately 500 or so blog posts could hold up today as being either accurate predictions (like Wheeler, I too was a big believer in WiMax) or final expressions of what I would have done as Chair of the FCC.

We certainly agree that Wheeler’s predictions of industry trends like WiMAX, in hindsight, are not deal breakers (although they should serve as reminders that one should avoid picking too many winners and losers). But at the same time, Wheeler’s words on policy matters in nearly 60 articles since 2007 should not be ignored, rationalized away, or dismissed either. In some sense, this is comparable to the vetting process for an appointee to the Supreme Court. To get a feel for the philosophy of an individual, both the White House and Congress pour over one’s writings and public opinions. Being asked to accept someone who can reshape public policy for years based on the personal recommendation of others only goes so far.

Many of Wheeler’s views are profoundly concerning, because they seem to betray a telecom industry conventional wisdom about the state of technology, wireless spectrum, regulation, and competition. His familiarity and comfort working within the paradigm of big cable and wireless is strongly contrasted with his suspicions and surprise regarding interlopers like Google and Apple — dubbed by Wheeler as part of a “Silicon Mafia.” We sense Wheeler seems most comfortable expecting to oversee business as usual, while advocating and accommodating some minor innovation here and there.

What is almost completely absent in most of Wheeler’s writings is the perspective of, or concern for ordinary consumers. What would Mr. and Mrs. Joe Average think about yet another consolidating merger between AT&T and one of its smaller competitors? What impact would another cable merger have on the bills paid by ordinary people in Colorado, Nebraska, or Pennsylvania? Is it good for consumers to advocate eliminating wireless network redundancy, as Wheeler does, after major events from 9/11 to Hurricane Sandy to the recent Boston Marathon attack all reveal wireless networks are susceptible to call volume clogging and extended service outages?

Tom Wheeler is an admirer of AT&T’s top-lobbyist Jim Cicconi.

More importantly, we are disturbed by Wheeler’s perspective about wired infrastructure that could have a major impact on the near future of rural telecommunications. Wheeler comes dangerously close to AT&T’s sentiments about its yesteryear rural landline network and its wish to switch those customers to wireless (with all the added costs, usage caps, and coverage issues). We cannot help but notice Wheeler frames the general issue much like AT&T does: an “evolution” that represents “weaning ourselves” from “the old wireline.” Ask yourself if AT&T is more or less comfortable knowing Mr. Wheeler’s attitudes about its wired telephone network. AT&T considers it an outdated money-loser and a nuisance in its rural service areas. Wireless is a license to print money, just as soon as the FCC and state regulators give the green light to go ahead. Is Wheeler to be the deciding vote?

We Don’t Believe Wheeler is an ‘Industry Plant’

Harold writes:

But while it is important to ask the right questions and give no one a free pass, it is equally important to evaluate the answers and the evidence fairly and accept their logical conclusions. The evidence that Wheeler would have approved the AT&T/T-Mobile merger had he actually been Chairman (rather than playing pundit) is pretty weak. To take that a step further and say that Wheeler’s justification for approving the merger as a means of reregulating the wireless industry was mere sham to hide his true sympathies seems to me exceedingly unjustified.

That mischaracterizes our sentiments about Mr. Wheeler. We do not believe he is some secret industry plant that is itching to deregulate the agency into a stupor. Nor do we believe a theoretical vote in favor of the AT&T/T-Mobile merger is evidence he is in AT&T’s back pocket specifically. Let us be clear: he served as a professional lobbyist for these companies for nearly 30 years. His job was to absorb and reflect the views of the nation’s biggest cable and phone companies both to politicians and regulators. Some remain friends and colleagues.

It is a safe bet most of the industry will welcome and celebrate Wheeler’s appointment. Many know him personally. Many others will feel safe that he is a reachable industry insider already familiar with the issues that concern them. This is what makes the D.C. revolving door so insidious. When you move from the regulated to the regulator (and back again), the only real outsiders are average consumers.

Here is an example of Wheeler admiring AT&T’s prowess in the early days of its attempted merger with T-Mobile. Notice how he characterizes the deal’s opponents:

“The most important times in any merger approval process are the first two weeks when the acquiring company gets to define the discussion and the last four weeks when the concerns raised by others and the analysis by the government congeals to define the issues to be negotiated in the final outcome. AT&T shot out of the blocks brilliantly, framing their action in terms of the spectrum shortage and President Obama’s desire to provide wireless broadband to rural areas. Over the coming months those who were caught by surprise, as well as those who would use the review process to gain their own advantages, will have organized to present their messages.”

Wheeler shows no evidence of being the FCC’s version of a game-changer like Elizabeth Warren. Instead, he’s an avowed admirer of AT&T’s top lobbyist Jim Cicconi. What will that difference mean? The New York Times, reporting more broadly on the problem of D.C.’s revolving door, provides some valuable clues:

Government officials and lobbyists agree that former agency officials have a much easier time getting phone calls or e-mail messages returned from their old colleagues, and that access often extends to greater credibility in arguing their clients’ positions.

One corporate lobbyist who worked as a regulator, asked whether he believed he had an inside edge in lobbying his ex-colleagues, said: “The answer is yes, it does. If it didn’t, I wouldn’t be able to justify getting out of bed in the morning and charging the outrageous fees that we charge our clients, which they willingly pay.”

The lobbyist, who spoke on condition of anonymity because of concerns about alienating government officials, added that “you have to work at an agency to understand the culture and the pressure points, and it helps to know the senior staff.”

Not quite

The most likely outcome of a Wheeler nomination is that he will be quickly approved, maintain the agency’s relatively low profile, and avoid rocking the boat too much. Even he doubts the power of the FCC to effect regulatory change unless those regulated volunteer to submit to more regulation. That means more quid pro quo agreements attached to mergers, acquisitions, and other deals the industry brings the FCC for approval. But as this quote illustrates, the industry remains in the driving seat:

“[…] Jim Cicconi sits astride a process that could determine the future of wireless policy, first for AT&T and then by extension for everyone else. Quite possibly the result of this merger decision will be far wider than the merger itself. At the end of the day we may be talking about a new era of wireless policy based on the Cicconi Commitment.”

Wheeler argued that the inability of the FCC to muster the political will to deal effectively with net neutrality and other broadband regulation made a consent decree around AT&T/T-Mobile the best way to update consumer protection rather than leave these services essentially unregulated.

Wheeler’s recognition of the inability of the FCC to get virtually anything done comes with no assurance he will do any better. Harold himself admits that the FCC’s track record of enforcement is “pathetic.” Has Wheeler written on his blog that he would seek to change that?

Wheeler’s reflections on the failed T-Mobile/AT&T merger present a clear sign he considers it a missed opportunity, with the usual voluntary divestiture of certain assets here and there with time limited pre-conditions that carry all the impact of one of those class action settlements that nets consumers a coupon or a $2 refund. Everybody but consumers walk away winners.

The Justice Department’s antitrust division, in contrast, illustrated the usefulness of a backbone when it quickly declared the merger proposal monstrously anti-consumer and anti-competitive and announced it would sue to stop it. Deal over and dead. When is the last time the FCC issued such a clear-cut, high-profile decision all on its own? Why is it so hard for the FCC to see the same anti-competitive nightmare so visible at the Department of Justice? Public Knowledge and other consumer groups saw the dangers from day one. Does Mr. Wheeler agree with the Justice Department or does he think he can do business with that shrewd AT&T lobbyist Jim Cicconi to get such deals approved the ‘right way?’

Our view remains the country and the Obama Administration could do far better choosing someone to lead the FCC that has not made a career lobbying for big cable and phone companies. If we want to solve America’s rural broadband problems, enforce fair billing practices and Net Neutrality, find new creative ways to utilize and distribute wireless spectrum, and promote competition while restricting industry consolidation, would we do better choosing an ex-industry lobbyist or an engineer, network planner, professional regulator, or an antitrust attorney?

President Obama went with the ex-lobbyist.

Subscribe

Subscribe AT&T announced late Friday it was acquiring Leap Wireless for almost $1.2 billion — a premium of 88 percent over Leap’s stock price.

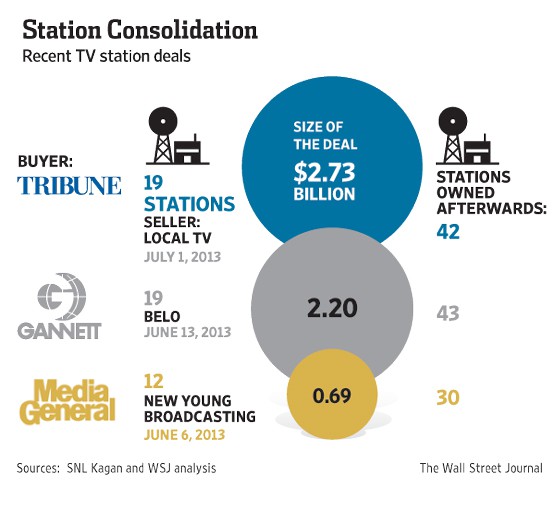

AT&T announced late Friday it was acquiring Leap Wireless for almost $1.2 billion — a premium of 88 percent over Leap’s stock price. It expects to pay off the loans and generate returns from the “significant free cash flow” generated by the stations.

It expects to pay off the loans and generate returns from the “significant free cash flow” generated by the stations. Tribune is not alone bulking up the number of stations they own and control. Last month Gannett nearly doubled its portfolio from 23 to 43 stations with the acquisition of Belo’s TV stations for $1.5 billion in cash and agreeing to cover $715 million in accumulated debt.

Tribune is not alone bulking up the number of stations they own and control. Last month Gannett nearly doubled its portfolio from 23 to 43 stations with the acquisition of Belo’s TV stations for $1.5 billion in cash and agreeing to cover $715 million in accumulated debt.

Malone also thinks it is time to discard reliance on cable television to bring home the revenue and profits Wall Street expects. The industry should instead turn its earning attention to broadband, a product few Americans can live without. Malone believes the cable industry is not only positioned to control content distributed on its TV Everywhere online video platform for authenticated cable subscribers, but also have a say in competing content from Netflix, among others, which are totally reliant on the broadband pipes provided by ISPs.

Malone also thinks it is time to discard reliance on cable television to bring home the revenue and profits Wall Street expects. The industry should instead turn its earning attention to broadband, a product few Americans can live without. Malone believes the cable industry is not only positioned to control content distributed on its TV Everywhere online video platform for authenticated cable subscribers, but also have a say in competing content from Netflix, among others, which are totally reliant on the broadband pipes provided by ISPs. Among the top recipients: Comcast, which collects $25-30 million a year and Time Warner Cable, which nets “tens of millions of dollars” from Google, Microsoft, and Facebook.

Among the top recipients: Comcast, which collects $25-30 million a year and Time Warner Cable, which nets “tens of millions of dollars” from Google, Microsoft, and Facebook.

But the most obvious foreshadowing of a big deal with Time Warner would most likely come if Charter first successfully acquires always-rumored-for-sale Cablevision, where the controlling Dolan family is rumored to be holding out for an exceptionally attractive buyout package other cable companies aren’t willing to offer. Time Warner itself has been rumored as a buyer, but current management has repeatedly stressed it will not pay a premium price for acquisition targets.

But the most obvious foreshadowing of a big deal with Time Warner would most likely come if Charter first successfully acquires always-rumored-for-sale Cablevision, where the controlling Dolan family is rumored to be holding out for an exceptionally attractive buyout package other cable companies aren’t willing to offer. Time Warner itself has been rumored as a buyer, but current management has repeatedly stressed it will not pay a premium price for acquisition targets.