In North America, the best prices, rebates and packages are only available to new customers while customer loyalty is rewarded with rate hikes.

In the United Kingdom, Virgin Media handles things differently, offering its best new packages and deals first to current customers before they become available to the public at large.

This week, the cable operator introduced two discounted “quad-play” bundles of broadband, mobile, television, and home phone service at prices that are unbelievably low by North American standards.

The $59.40 Big Bang bundle provides 100Mbps broadband, a Virgin Media TiVo, home phone service, and Virgin Mobile service with unlimited talk/text and 250MB of data;

The $84.88 Big Kahuna delivers 152Mbps broadband, a Virgin Media TiVo with a 230 TV channel package, home phone service, and Virgin Mobile service with unlimited talk/text and 250MB of data.

“Our fantastic new bundles deliver unprecedented value as standard,” said Dana Strong, chief operating officer of Virgin Media. “For the first time, households will be able to get the best broadband together with the UK’s best value mobile SIM, as part of a bundle perfectly tailored to the customer’s needs.”

Virgin Media will introduce other packages in the near future and is resetting its standard broadband speed offering to 50Mbps. Customers with 30Mbps will be upgraded to 50Mbps, 60Mbps customers will soon get 100Mbps, and 120Mbps customers will be boosted to 152Mbps — all at no additional charge.

The new bundles come with an 18-month contract and do not include the usual BT line rental charge for telephone service that most landline customers in Britain already pay, regardless of provider, which costs an extra $27.15 a month.

Customers who don’t want mobile service with Virgin will be given a further discount, as the price chart below shows:

Virgin Media bundle deal

Price

Line Rental

Total Monthly Price

Virgin Media Big Bang – 100Mbps broadband, Virgin Media TiVo, home phone

$50.92/month

$27.15/month

$78.07/month

Virgin Media Big Bang – 100Mbps broadband, Virgin Media TiVo, home phone, Virgin mobile SIM-only

$59.40/month

$27.15/month

$86.55/month

Virgin Media Big Kahuna – 152Mbps broadband, Virgin Media TiVo, home phone

$76.38/month

$27.15/month

$103.53/month

Virgin Media Big Kahuna – 152Mbps broadband, Virgin Media TiVo, home phone, Virgin mobile SIM-only

After months of fruitless discussions with cell phone carriers, the U.S. Senate is moving closer towards legislation that would stop phone companies from blocking “kill switch” technology that could disable lost or stolen phones, discouraging would-be thieves.

Sen. Amy Klobuchar (D-Minn.) sent letters this week to Verizon Wireless, AT&T, Sprint and T-Mobile asking the carriers to do more to protect customers from phone theft.

Klobuchar is concerned wireless companies may be blocking cell phone manufacturers from enabling anti-theft technology customers could activate to disable missing phones and prevent unauthorized access or reactivation without the customer’s consent.

“Mobile devices aren’t just telephones anymore – increasingly people’s livelihoods depend on them,” Klobuchar said. “That’s why we need to do more to crack down on criminals who are stealing and reselling these devices, costing consumers billions every year. The wireless industry needs to step up to the plate and address these thefts, and make sure consumers have the most advanced security technology at their fingertips.”

The technology is already widely available internationally and has dramatically reduced smartphone theft by eliminating most of the resale value of the expensive devices, which are rendered useless once the phone is disabled.

Apple has contractual control over its products unlike most cell phone manufacturers.

But American carriers have so far refused permission to allow manufacturers like Samsung to introduce the feature in North America. Apple has successfully introduced a “kill switch” on many of its latest devices thanks to favorable contractual language that limits outside interference with the software Apple develops for its wireless devices. Other manufacturers are generally required to bow to carrier demands.

“I think that this is motivated by profit,” San Francisco district attorney George Gascon told CNN. Gascon reported he had seen e-mails from carriers that rebuffed Samsung’s efforts to introduce the technology in the American market.

Companies like AT&T claim that a “kill switch” feature could be exploited by hackers and make restoring service extremely difficult. But manufacturers and proponents of kill switch technology dismiss that argument, claiming the process is easily reversible once a customer enters a correct name and password. Critics believe carriers are motivated by the potential loss of millions from the sale of insurance plans, replacement phones, and the increased revenue earned from the reactivation of stolen phones.

With more than 1.6 million smartphones stolen or lost annually, carriers sell more than $800 million of replacement phones worth at least $500 each. Wireless phone companies also profit selling insurance plans priced at $7 or more monthly that offer free or discounted, typically refurbished cell phone replacements. Most customers never use the insurance plans, earning providers an extra $84 a year in revenue per customer.

Without kill switch technology and other theft prevention measures, the incentive to steal valuable smartphones continues to increase. As the price of sophisticated smartphones continues to increase, they are a prime target in street crime incidents. In San Francisco, 67% of robberies are related to mobile devices, according to the police department. Ten percent of phone owners have had a phone stolen, according to a Harris poll.

For now, the industry has only agreed to develop a voluntary database of phones reported lost or stolen. But participating carriers are largely American, allowing crooks to bypass the list by exporting phones overseas where they are quickly reactivated.

Klobuchar wants carriers to go on the record about kill switch technology, and her letter requested a formal response to three questions:

Whether companies received offers from handset manufacturers to install “kill switch” technology;

Have companies introduced the technology and, if not, why not;

How companies will introduce such technology in the future.

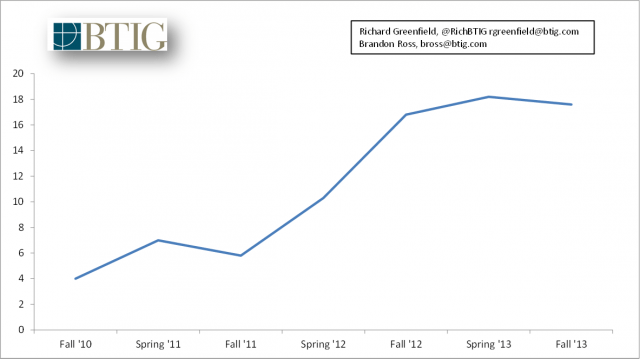

The median bandwidth use slowdown (Image: BTIG Research)

Despite perpetual cries of Internet brownouts, usage blowouts, and data tsunamis that threaten to overwhelm the Internet, new data shows broadband usage has leveled off in North America, undercutting providers’ favorite excuse for usage limits and consumption billing.

Sandvine today released its latest broadband usage study, issued twice yearly. The results show a clear and dramatic decline in usage growth in North America, with median usage up just 5% compared to the same time last year. That is a marked departure from the 190% and 77% growth measured in two earlier periods. In fact, as Richard Greenfield from BTIG Research noted, mean bandwidth use was down 13% year-over-year, after the second straight six month period of sequential decline.

Companies like Cisco earn millions annually pitching network management tools to providers implementing usage caps and consumption billing. For years, the company has warned of Internet usage floods that threaten to make the Internet useless (unless providers take Cisco’s advice and buy their products and services).

“Demand for Internet services continues to build,” said Roland Klemann from Cisco’s Internet Business Solutions Group. “The increasing popularity of smartphones, tablets, and video services is creating a ‘data tsunami’ that threatens to overwhelm service providers’ networks.”

Providers typically use “fairness” propaganda when introducing “usage based pricing,” blaming exponential increases in broadband usage and costly upgrades “light users” are forced to underwrite. A leveling off in broadband usage undercuts that argument.

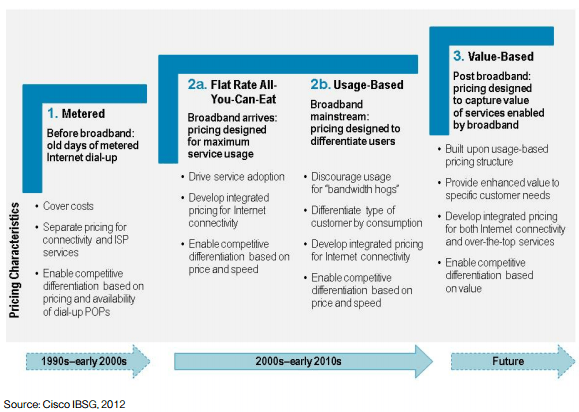

In 2011, broadband services became mainstream in developed countries, with fixed-broadband penetration exceeding 60 percent of households and mobile broadband penetration reaching more than 40 percent of the population in two-thirds of Organisation for Economic Co-operation and Development (OECD) countries.

Meanwhile, traditional voice and messaging revenues have strongly declined due to commoditization, and this trend is expected to continue. Therefore, operators are now relegated to connectivity products. The value that operators once derived from providing value-added services is migrating to players that deliver services, applications, and content over their network pipes.

As if this were not enough, Internet access prices are dropping, sales volumes are declining, and markets are shrinking. The culprit: flat rate “all-you-can-eat” pricing. Such a model lacks stability—sending service provider pricing into a downward spiral—because it ignores growth potential and shifts the competition’s focus from quality and service differentiation to price.

While Klemann was spouting warnings about the dire implications of a data tsunami, Cisco’s White Paper quietly told providers what they already know:

Maximum Profits

“[Wired] broadband operators should be able to sustain forecasted traffic growth over the next few years with no negative impact on margins, as the incremental capital expenses required to support it are under control.”

If usage limits and consumption billing are not required to manage data growth or cover the cost of equipment upgrades, why adopt this pricing? The potential to exploit more revenue from mature broadband markets that lack robust competition.

“In light of the forecasted Internet traffic growth mentioned earlier and competitiveness in the telecommunications market, Cisco believes that fixed-line operators should consider gradually introducing selected monthly traffic tiers to sustain [revenue], while a) signaling to customers that “traffic is not free,” and b) monetizing bandwidth hogs more sustainably.”

Cisco makes its recommendation despite knowing full well from its own research that customers hate usage-based pricing.

“The introduction of traffic tiers and caps—especially for fixed broadband services—is not welcomed by the majority of customers, as they have learned to ‘love’ flat rate all-you-can-eat pricing. Most customers consider usage-based pricing for broadband services ‘unfair,’ according to the 2011 Cisco IBSG Connected Life Market Watch study.”

Cisco teaches providers how to price broadband like trendy boutique bottled water and blame it on growing Internet usage.

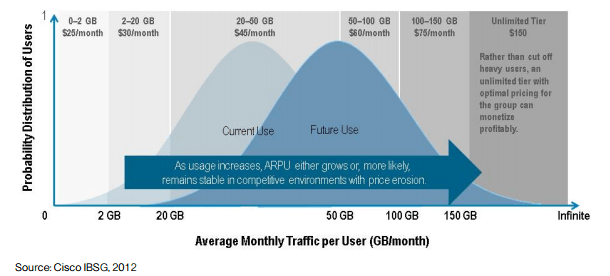

But with competition lacking, Cisco’s advice is to move forward anyway, as long as providers initially introduce caps and consumption billing at prices that do not impact the majority of customers… at first. In uncompetitive markets, Cisco predicts customers will eventually pay more, boosting provider revenue. Cisco’s “illustrative example” of usage billing in practice set prices at $45 a month for up to 50GB of usage, $60 a month for 50-100GB, $75 for 100-150GB, and $150 a month for unlimited access — more than double what customers typically pay today for flat rate access.

Usage billing arrives right on time to effectively handle online video, which increasingly threatens revenue from cable television packages.

Sandvine’s new traffic measurement report notes the increasing prominence of online video services like Netflix, YouTube, Hulu, and Amazon Video.

“As with previous reports, Real-Time Entertainment (comprised of streaming video and audio) continues to be the largest traffic category on virtually every network we examined, and we expect its continued growth to lead to the emergence of longer form video on mobile networks globally in to 2014,” Sandvine’s report noted.

Sandvine found that over half of all North American Internet traffic during peak usage periods comes from two services: Netflix and YouTube. YouTube globally is the leading source of Internet traffic in the world, according to Sandvine.

An old excuse for usage caps on “data hogs” – peer-to-peer file-sharing, continues its rapid decline towards irrelevance, now accounting for less than 10 percent of total daily traffic in North America. A decade earlier, file swapping represented 60 percent of Internet traffic.

Cisco’s answer for the evolving world of popular online applications is a further shift in broadband pricing towards “value-based tiers” that monetize different online applications by charging broadband users extra when using them. Cisco is promoting an idea that well-enforced Net Neutrality rules would prohibit.

Citing the bottled water market, Cisco argues if some customers are willing to pay up to $6 for a liter of trendy Voss bottled water, flat rate “one price fits all” broadband is leaving a lot of money on the table. With the right marketing campaign and a barely competitive marketplace, providers can charge far higher prices to get access to the most popular Internet applications.

“Research from British regulator Ofcom shows that consumers are becoming ‘addicted’ to broadband services, and heavy broadband users are willing to pay more for improved broadband service options.”

Wharton School professors Jagmohan Raju and John Zhang concluded price is the single most important lever to drive profitability.

The political implications of blaming phantom Internet growth and manageable upgrade costs for the implementation of usage caps or usage-based billing is uncertain. Even the “data hog” meme providers have used for years to justify usage caps is now open to scrutiny. Sandvine found the top 1% of broadband users primarily impact upstream resources, where they account for 39.8% of total upload traffic. But the top 1% only account for 10.1% of downstream traffic. In fact, Apple is likely to provoke an even larger, albeit shorter-term impact on a provider’s network from software upgrades. When the company released iOS7, Apple Updates immediately became almost 20% of total network traffic, and continued to stay above 15% of total traffic into the evening peak hours, according to Sandvine.

Some other highlights:

Average monthly mobile usage in Asia-Pacific now exceeds 1 gigabyte, driven by video, which accounts for 50% of peak downstream traffic. This is more than double the 443 megabyte monthly average in North America.

In Europe, Netflix, less than two years since launch, now accounts for over 20% of downstream traffic on certain fixed networks in the British Isles. It took almost four years for Netflix to achieve 20% of data traffic in the United States.

Instagram and Dropbox are now top-ranked applications in mobile networks in many regions across the globe. Instagram, due to the recent addition of video, is now in Latin America the 7th top ranked downstream application on the mobile network, making it a prime candidate for inclusion in tiered data plans which are popular in the region.

Netflix (31.6%) holds its ground as the leading downstream application in North America and together with YouTube (18.6%) accounts for over 50% of downstream traffic on fixed networks.

P2P Filesharing now accounts for less than 10% of total daily traffic in North America. Five years ago it accounted for over 31%.

Video accounts for less than 6% of traffic in mobile networks in Africa, but is expected to grow faster than in any other region before it.

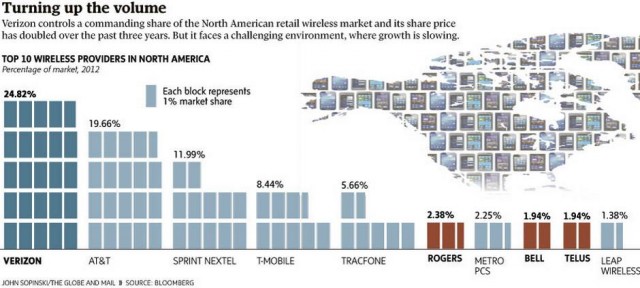

The three companies that control 90 percent of Canada’s cell phone marketplace have set what they argue is ‘cut-throat’ competition aside to team up in a multi-million dollar lobbying campaign to discourage Verizon Wireless from entering the country.

Bell, Rogers, and Telus have maintained what critics charge is a “three-headed oligopoly” in the wireless business for years, leading to findings from the OECD that Canada is among the ten most expensive countries in the world for wireless service in almost every category and has among the highest roaming rates in the world.

Americans also pay high cell phone prices, and customers of both countries will find somewhat comparable pricing when comparing prices north or south of Lake Ontario. A shopper in Niagara Falls, N.Y. can find the Samsung Galaxy S4 from a Verizon reseller for $120 with a two-year contract. A shared data service plan runs as little as $80 a month for 500MB of data and unlimited domestic calling and global texting. Travel across the Rainbow Bridge to Niagara Falls, Ontario, walk into a Rogers store and the same phone runs $199 with a two-year contract (most Canadian carriers used to offer three-year contracts until the government banned them earlier this year) and a service plan running $80 a month offering the same 500MB of data and unlimited domestic calling and texting. Rogers charges extra if customers want to text a customer outside of Canada, however.

Verizon is no discount carrier. Verizon management has repeatedly stressed it offers premium service and coverage and can charge commensurately higher prices for access to that network. So the idea that Verizon’s interest in entering Canada is to launch a vicious price war is suspect, according to many telecommunications analysts.

Keep Verizon out of Canada at all costs!

They are coming.

In June, the Globe and Mail reported Verizon had shown serious interest in acquiring Canadian cellular upstart Wind Mobile with an early bid of $700 million. Wind Mobile, one of the three significant new “no-contract” entrants vying for a piece of the country’s cell phone market, has limped along since opening for business in 2009, unable to attract much interest from customers concerned about coverage gaps and the poor choice of mobile devices.

More recently, Wind Mobile’s new owner — the Russian mobile giant Vimpelcom — has expressed an interest in selling off the carrier because it cannot gain traction against the biggest three, which also control 85 percent of mobile wireless spectrum.

News that Verizon had taken an interest in the carrier leveled shock waves across the Canadian financial markets. Shares in the three largest telecom giants fell sharply on the news. Earlier this month, Bell CEO George Cope reported that Bell, Telus and Rogers have taken a $15-billion cumulative hit on the capital markets since Verizon hinted interest in Wind Mobile.

[flv width=”480″ height=”290″]http://www.phillipdampier.com/video/CBC Verizon takes aim at telecom Big 3 with possible Wind Mobile bid 8-19-13.flv[/flv]

The CBC reported earlier this summer that Verizon Wireless was interested in acquiring the 600,000 customers of independent wireless provider Wind Mobile, which has an insignificant share of the Canadian wireless market. (2 minutes)

Spending a few million, or even a billion dollars, to keep Verizon south of the Canadian-U.S. border is well worth it to the three big players who have launched an expensive campaign to block the proposed transaction and are willing to pay premium prices to keep struggling carriers from being sold to deep-pocketed American telecom companies.

Telus had already done its part, attempting to scoop up another scrappy upstart carrier that wanted out of the wireless business. But the Canadian government rejected Telus’ proposed acquisition of Mobilicity, claiming it would harm efforts to expand Canadian wireless competition. Not to be deterred, Rogers is now attempting a cleverly structured deal to acquire Wind Mobile out from under Verizon with a proposed buyout worth more than $1 billion.

To avoid the anticipated rejection of the deal by Canadian regulators on competition grounds, Rogers has reportedly joined forces with Toronto-based private equity firm Birch Hill Partners that would make that firm the owners-in-name. Although Rogers wouldn’t get a direct equity stake in Wind, it would finance a good part of the deal and win access and control of Wind’s mobile spectrum for its own network. More importantly, it could keep Verizon out of Canada.

“The government is handing out loopholes to Verizon to beg them into Canada”

Cell phone companies in Canada are particularly angry that the government has set aside certain spectrum and guaranteed access for upstart providers to successfully establish themselves without having to outbid the cash-rich big three for wireless frequencies or have to build a nationwide network from scratch. Bell, Rogers and Telus have consistently opposed spectrum set-asides for small carriers, deeming them “unfair.” They argue Canadians’ voracious needs for more wireless service are unending, and it would be unfair not to sell the spectrum to benefit their larger customer bases. But hearing that Verizon, a company larger than Bell, Rogers, and Telus combined, could get preferential treatment and spectrum to enter the country has them boiling mad.

Bell’s CEO George Cope appeared on “The Lang and O’Leary Exchange” to debate the fairness of Verizon’s possible entry into Canada’s wireless market. Cope argues Verizon is getting special favors. (9 minutes)

Cope

The idea of luring a company to move or begin offering service in a barely competitive marketplace is hardly new. Cities have offered preferential policies to airlines to fly in and out of particular cities, local governments have offered tax abatements to get companies to set up shop, and providing exemptions for zoning and infrastructure have been familiar to telecommunications companies for decades.

In 1880, the National Bell Telephone Company had incorporated, through an Act of Parliament, the Bell Telephone Company of Canada (today also known as BCE), which was given the right to build telephone lines over and along all public property and rights-of-way without compensation to the public or former owners. Through a series of mergers and acquisitions, Bell would later become the dominant monopoly provider of telephone service across much of eastern Canada.

When the phone companies were handed wireless spectrum to launch their wireless businesses in the 1980s, they didn’t have anything to complain about either.

None of that history impressed Bell’s current CEO George Cope, who took to the airwaves to complain Verizon was being given preferential treatment:

Verizon could bid on two blocks of Canadian spectrum set aside for new entrants to the market in auction later this year. Because the big three Canadian firms are not permitted to bid on these blocks, they are likely to be sold at a lower price.

Verizon would not have to build its own networks to remote or rural communities, but would be able to piggyback on existing networks.

Verizon can bid to acquire small Canadian companies such as Mobilicity or Wind, but Bell, Telus and Rogers are forbidden from bidding on them.

“A company of this size certainly doesn’t need handouts from Canadians or special regulatory advantages over Canadian companies,” Bell said in a full-page newspaper ad. “But that is exactly what they get in the new federal wireless regulations. We’re ready to compete head to head, but it has to be a level playing field,” Cope said in a TV interview, echoing Rogers CEO who also called for a “level playing field.”

[flv width=”640″ height=”380″]http://www.phillipdampier.com/video/CBC Is Verizon really the bogeyman Canada’s telecom giants claim 8-19-13.flv[/flv]

Bell, Telus, and Rogers have launched a lobbying campaign designed to make life difficult for Verizon Wireless if it chooses to enter Canada. The CBC reports Verizon will be able to bid on more spectrum than Canadian carriers and will have the right to roam on Canada’s incumbent wireless networks. (2 minutes)

Industry Minister Moore

Telus went further, claiming Verizon’s entry into Canada would result in a “bloodbath” for Canadian workers, laid off by the three largest Canadian providers to cut costs to better compete with Verizon.

But Cope said at least one Canadian carrier won’t be able to compete at all, because preferential treatment for wireless spectrum will result in at least one of the big three to lose at a forthcoming spectrum auction, guaranteeing degraded wireless broadband speeds and worse service.

The three companies have found little sympathy in Ottawa, particularly from Industry Minister James Moore, now on a road tour across Canada to promote the government’s wireless competition policies. He called the big three’s loud campaign self-serving and announced a new website sponsored by the Conservative Party of Canada to prove it.

“I think that the public instinctively knows that when they have more choices that prices go down and more competition they’re well served by that,” he told CBC News in Vancouver on Monday. “The noise that we’re hearing is about you know companies trying to protect their company’s interest. Our job as a government is larger than that, our job is to serve the public interest and make sure that the public is served in this so that’s one of the reasons why I’m pushing back a little bit.”

Industry Minister James Moore appeared on CBC Radio this morning to contest the wireless industry’s claims that Verizon is getting special treatment and will bring unfair competition to the Canadian wireless market. (7 minutes)

You must remain on this page to hear the clip, or you can download the clip and listen later.

Oppose Verizon Wireless. Do it for Canada!

But the wireless companies show no signs of backing down and have turned towards appealing to Canadian nationalism and fairness.

“The U.S. government is not giving Canadian wireless carriers any special access to the U.S. market,” says a website launched by the big three cell providers to drum up support for a “level playing field.” “Then why is it that our own government is giving American companies preferential treatment over our own companies?”

This week, a Reuters report citing unnamed sources suggests Bell, Telus, and Rogers are about to target Verizon directly with a new campaign warning Canadians the American giant has been implicated in allowing the U.S. government open access to network and customer data, which would represent a profound privacy threat to Canadian customers.

[flv width=”640″ height=”380″]http://www.phillipdampier.com/video/Bell Rogers Telus Ad 8-13.flv[/flv]

Bell, Telus, and Rogers paid to produce this ad calling on Canadians to protest unfair competition from an American wireless company. (1 minute)

So far, Canadians’ hatred of their telecommunications providers has trumped the companies’ public relations and scare tactics. The Conservative government in Ottawa is winning support for its wireless competition war, even from unlikely places.

“Someone mark the date,” Tweeted one Halifax woman not inclined to vote Conservative. “Stephen Harper has done something I mostly support.”

“Eat it Telus/Bell/Rogers,” wrote a Calgary man fed up with the lack of competition in Canadian wireless.

John Lawford, executive director of the Public Interest Advocacy Centre in Ottawa, says opposition from the big three telecom companies is obvious because they don’t want to face a fourth, powerful competitor.

“They should be scared because chances are they’re going to have more competition in the Canadian market if Verizon comes in and they are going to have to lower their prices and compete harder,” Lawford told CBC News. “It’s pretty rich of them to be talking about unfairness” when they already control 90 per cent of Canadian spectrum, he added.

Iain Grant of the SeaBoard Group, a telecommunications consultancy, said government policies to open up more competition are designed to shake things up.

“[The new rules weren’t] meant to be a level playing field,” said Grant. “[They were] meant to give a leg up [to new competitors].”

“To talk of loopholes, as some do, is to not understand that the same companies who complain most loudly about loopholes in 2013 were the recipients of even greater public largesse in 1985 when the government gifted their initial spectrum as an incentive to build a wireless business in Canada,” said Grant.

Few companies have taken on the Canadian big three telecom providers because of their enormous market share, at least inside Canada.

Nine out of ten Canadian wireless users are subscribed to Bell, Telus or Rogers. Trying to convince a banker to extend capital loans to effectively confront a wireless oligopoly in a country with an enormous expanse of land but not people and find enough airwaves among the 15% not controlled by the big three is an uphill battle.

[flv width=”640″ height=”380″]http://www.phillipdampier.com/video/CBC Wireless war heats up 8-19-13.flv[/flv]

CBC reports Industry Minister Moore believes increasing competition is the best way to cut Canadian cell phone bills. Regardless of whether Verizon enters Canada, the current government will continue to push for more competition. Even the threat of Verizon coming to Canada has already reduced prices. (2 minutes)

Why does Verizon want to enter Canada?

Analysts suspect Verizon’s interest in Canada has little to do with wooing Canadians to Big Red. Many suspect Verizon’s true interest is to make life easier for its traveling American customers who head north for business or pleasure.

Chief among the possible benefits is the elimination of roaming charges for Verizon customers.

“Verizon’s customers come into the country every day through all the bridges and ports of entries and they want to roam where they want to roam, whether that’s fishing in Saskatchewan or hunting in northern Ontario or wherever,” said Grant.

There are other apparent impediments that could limit the usefulness of Wind’s mobile network to Verizon. In addition to only operating in the largest Canadian cities, Wind’s infrastructure is built by Chinese firm Huawei and is not compatible with Verizon’s technology.

Huawei has been the subject of significant controversy because of its reported ties to the Chinese military. Fears that data could be intercepted by the Chinese government have kept many North American firms from doing business with the company.

Verizon also lacks bundling options for Canadian customers. The biggest three Canadian providers can offer telephone, television, and wired broadband service to their customers. Verizon can only offer wireless service.

Verizon has second thoughts

Perhaps most remarkable are late reports that Verizon may be having second thoughts about jumping into Canada’s wireless market.

Desjardins analyst Maher Yaghi said Verizon may have delayed its plans until after Ottawa’s auction of 700MHz spectrum planned for January to better understand the potential spectrum costs it will incur entering Canada.

Others speculate incumbent providers may be attempting to end the rationale for Verizon to enter Canada in the first place. One major development includes a much more favorable roaming deal for Verizon that could dramatically cut the costs for Verizon customers to roam on Canadian networks.

Regardless of what Verizon does, Industry Minister Moore says Canada’s goal of getting increased competition will continue.

CBC reports Verizon may be having second thoughts about entering Canada. Verizon may not be interested in entering a political battle to win licenses to provide service and may want to acquire its own spectrum before considering buying either Wind Mobile or another competitor like Mobilicity. (2 minutes)

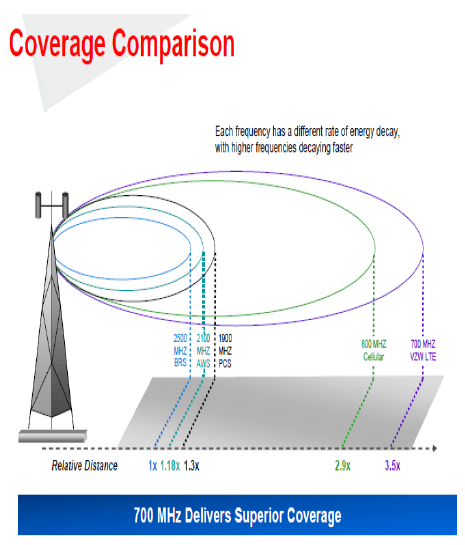

In the race to acquire spectrum and market share, AT&T and Verizon Wireless have already won most of the awards worth taking and have little to fear from smaller competitors. The U.S. government has seen to that.

The two wireless giants have benefited enormously from government spectrum auctions that award the most favorable wireless spectrum to the highest bidder, a policy that retards competition and guarantees deep-pocketed companies will continue to dominate in the coverage wars.

Winner-take-all spectrum auctions have already proven that AT&T and Verizon are best equipped to bid and win coveted 700MHz spectrum which provides the best indoor and fringe-area reception. This is why AT&T and Verizon customers often find “more bars in more places” than customers relying on Sprint or T-Mobile. Smaller carriers typically have to offer service over much-higher frequencies that don’t penetrate buildings very well. With a reduced level of service, these competitors are at an immediate competitive disadvantage. They also must spend more for a larger number of cell towers to provide uniform service.

Verizon’s own presentation materials tout the benefits of controlling 700MHz spectrum, which is less costly to deploy and offers more robust coverage.

Sprint and T-Mobile have two strikes against them at the outset — less favorable spectrum and much smaller coverage areas. Customers who want the best reception under all circumstances usually get it from the biggest two players. Those focused primarily on price are willing to sacrifice that reception for a lower bill.

The same story is developing in the wireless data marketplace. AT&T and Verizon Wireless have the strongest networks as Sprint and T-Mobile fight to catch up.

Where America Went Wrong: The Repeal of Spectrum Caps

Tom Wheeler: America’s #1 advocate for repeal of Spectrum Caps is now the chairman of the FCC.

Originally, the United States prevented excessive market domination with a “Spectrum Cap,” — a maximum amount of wireless spectrum providers could hold in any local market. The rule was part of the sweeping changes in telecommunications law introduced in the mid-1990s. Wireless spectrum auctions replaced lotteries or strict frequency assignments based on merit. The U.S. government promoted the auction system as a win for the U.S. Treasury, which has been promised $60 billion in proceeds from the wireless industry (not the amount actually collected) since auctions began in 1994.

The cost to U.S. consumers from increasing cell phone bills in barely competitive markets is still adding up.

After the auction system was introduced, the largest carriers acquired some of the most favorable, lower-frequency spectrum, easily outbidding smaller rivals. Most of the smaller regional carriers that ultimately won coveted 700MHz spectrum emerged victorious only when AT&T and Verizon felt the smaller markets were not worth the investment. In larger markets, spectrum caps were a gatekeeper against acquiring excess spectrum and, more importantly, rampant industry consolidation.

Under the pre-2001 rules, wireless companies couldn’t own more than 45MHz of spectrum in a single urban area or more than 55MHz in a rural area. That was when Verizon and AT&T competed with carriers that no longer exist — old familiar names like Nextel, Cingular, VoiceStream, Alltel, Centennial Communications, Qwest, and many others considered safe from poaching because the most likely buyers would find themselves over their spectrum limits.

As the largest carriers realized the caps were an effective merger/buyout firewall, the wireless industry began a fierce lobbying campaign against them. Leading the charge was Tom Wheeler, then-president of the CTIA Wireless Association, the nation’s top cellular industry lobbying group. Today he is chairman of the Federal Communications Commission.

“Today, America faces a severe spectrum shortage for wireless services,” Wheeler said in 2001. “The spectrum cap is a legacy of spectrum abundance, not shortages; the inefficiencies it perpetuates cannot be allowed to continue. While the U.S. government is looking for ways to catch up to the rest of the world on spectrum allocations, removal of the cap can at least increase the efficiency of existing spectrum.”

Former FCC Commissioner Michael Copps opposed retiring Spectrum Caps: “Let’s not kid ourselves: This is, for some, more about corporate mergers than it is about anything else.”

Wheeler was backed by an intensive lobbying effort funded by the largest wireless companies itching to merge and acquire.

By the end of 2001, the new Bush Administration’s FCC was ready to deal, gradually repealing the spectrum caps and fueling major wireless industry consolidation in the process. Providers everywhere could now own or control 55MHz of spectrum in any market, with the promise the caps would be repealed altogether by March 2003.

The result was already foreseen by former FCC Commissioner Michael Copps in November 2001, when he strongly dissented to the Republican majority gung ho for dissolving spectrum caps.

“Let’s not kid ourselves: This is, for some, more about corporate mergers than it is about anything else,” Copps wrote in his strong dissent. “Just look at what the analysts are talking about as the specter of spectrum cap renewal approaches – their almost exclusive focus is on evaluating the candidates for corporate takeovers and handicapping the winners and losers in the spectrum bazaar we are about to open.”

Just in case Copps might be making headway in his campaign to protect competition, Wheeler began complaining even louder about spectrum caps during the spring of 2003, just before their dissolution.

“The wireless industry fought long and hard to secure this spectrum for America’s wireless consumers,” said Wheeler. “Now we must tread carefully — in this era of rapid technological change, writing rules that are too restrictive would be irresponsible. In order to use this spectrum both efficiently and effectively, those who purchase this spectrum at auction must be allowed the freedom to grow and evolve with the demands of the market.”

Europe: Protecting Consumers from Giant Multinational Competition Consolidators (Some of the same ones AT&T reportedly wants to buy)

There is a reason Europeans are shocked by the costs of wireless service in the United States and Canada. North Americans pay higher prices for less service than our European counterparts. Most of the New World also has fewer choices in near-equivalent service providers.

Much of this difference can be attributed to European regulators maintaining focus on driving competition forward and disallowing rampant industry consolidation. But as Wall Street turns its attentions increasingly towards Europe to push for the next big wave of wireless mergers, the European system of “competition first” could be undermined if providers follow the North American model of high profits and reduced competition through consolidation.

Across much of Europe, at least four national carriers serve each EU member state, almost all controlling a share of the most valued, low-frequency wireless spectrum. European regulators do not allow a small handful of providers to maintain a stranglehold on the most valuable radio spectrum. Competitors have traditionally been offered a spectrum foundation to build networks that can stand up to their larger counterparts — the large multinationals or ex-state monopoly providers who had a head start providing service.

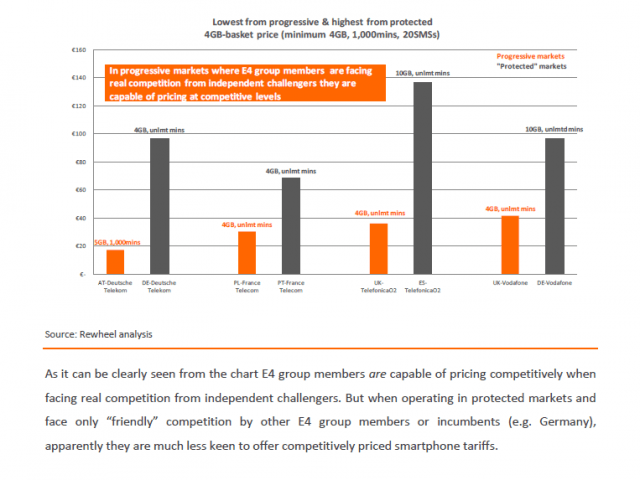

A report released by Finland market research firm Rewheel in May found clear evidence that the European model was benefiting consumers at the expense of rampant provider profits. Europeans in “progressive” markets that welcomed new competitive entrants pay lower prices for far more service. In some cases, the price differences between the five giant multinational providers that dominate Europe — Vodafone, KPN, France Telecom, Telefonica and Deutsche Telekom — were staggering. Competitors like Tele2, TeliaSonera, and “3” charge up to ten times less than the larger companies for equal levels of service.

[flv width=”640″ height=”380″]http://www.phillipdampier.com/video/Bloomberg ATT Takeover List of European Wireless Carriers 7-15-13.flv[/flv]

“Europe is ripe for competition,” reports Bloomberg News. Providers like AT&T may be preparing to embark on a European wireless acquisition frenzy, but Wall Street warns profits are much lower because of robust price competition in Europe that benefits consumers. (4 minutes)

The study also found a number of the largest European providers were following in the footsteps of Verizon Wireless, AT&T, Rogers, Bell, and Telus here in North America:

Prices were enormously higher in markets that lack effective competition from an upstart competitor able to deliver a comparable level of service. Smaller cell companies with very limited infrastructure or with non-favored spectrum could not provoke dominant players to cut prices because reception quality was starkly lower and consumers would have to cope with a reduced level of service. In Europe, when new competitors were able to fully build-out their networks using favorable spectrum, incumbents in these progressive markets slashed prices and boosted services to compete. In North America, upstart competitors cannot access favorable spectrum for financial reasons and the investor community has dismissed many of these players as afterthoughts, starving them of much-needed investment.

Large dominant European providers are now heavily lobbying for deregulation of merger and acquisition rules and want the right to acquire the competition entering their markets.

In almost half of the EU27 member state markets spectrum is utilized very inefficiently by the largest incumbent telco groups who are keen to protect their legacy fixed assets and cement their European dominance with more consolidation at the price of competition. In the United States and Canada, many of the largest providers crying the loudest for more wireless spectrum have still not used the spectrum already acquired.

From the Finnish report:

The obvious question that needs to be asked is how is it technologically possible and economically viable for Tele2, 3 and TeliaSonera to offer four times more gigabytes of data usage at a fraction of the price charged by larger companies.

Do independent challengers have privileged access to more efficient technologies (i.e. LTE) than the E4 group members?

Do they hold relatively more spectrum capacity than the E4 group members?

Do independent challengers have access to more radio sites and their spectrum reuse factor is higher than the E4 group members?

Or are independent challengers (i.e. Tele2, DNA) unprofitable?

None of the above are true.

The answer is actually very simple. Independent challengers and incumbents such as TeliaSonera present mainly in progressive markets are utilizing the spectrum resources assigned to them. In contrast, incumbent telco groups […] rather than utilizing their spectrum resources instead appear to be more concerned about keeping the unit price of mobile data very high […] by restricting supply, the same way the lawful “cartel” of OPEC controls the price of oil by turning the tap off.

In progressive markets (where at least one independent challenger is present, triggering spectrum utilization competition) such as Finland, Sweden, Austria and the UK, mobile data consumption per capita is up to ten times higher than in protected markets.

In some European countries dominated by the biggest players, consumers are being gouged for service. Where robust competition exists, prices are dramatically lower.

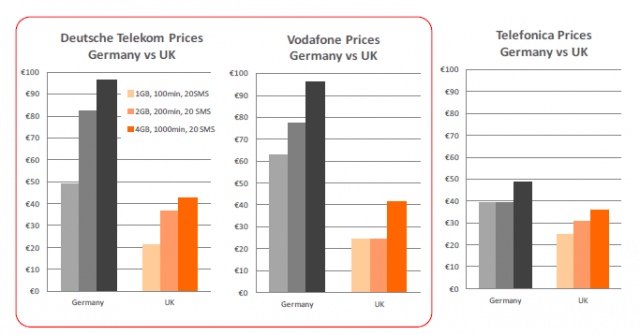

The European nation where market conditions are most similar to the United States is Germany. Two large carriers dominate the market: Deutsche Telekom, the former state-owned telephone company and Vodafone, part owner of Verizon Wireless.

In Germany, consumers spending €20 ($26) end up with a data plan offering as little as 200MB of usage per month. In progressive markets in adjacent countries, spending the same amount will buy an unlimited use data plan or at least one offering tens of gigabytes of usage. In short, German smartphone service is up to 100 times more restrictive than that found in nearby Scandinavia or in the United Kingdom. These same two companies charge Germans double what English customers pay and a Berliner will end up with 22 times less data service after the bill is settled.

So what is going on in Germany that allows the marketplace to stay so price-distorted? The fact all four significant competitors have close ties to or are owned by the large multinational telecom operators mentioned above. Deutsche Telekom, Vodafone, Telefonica and E-Plus, the latter one belonging to the Dutch KPN Group are all members of a lobbying organization attempting to persuade the EU to invest public funds into improving Europe’s wired broadband networks. Playing against that proposition is a growing number of Europeans moving to wireless. By charging dramatically higher wireless prices in Germany, all four companies have successfully argued that wireless adoption is not a significant reason to stall public financing of private broadband projects. In fact, Germany’s wireless growth is well below other EU nations.

The Finnish researchers point out the evidence of informal provider collusion is pretty stark in Germany:

“One would expect these ‘European Champions,’ especially the ones with lower market shares (Telefonica and E-Plus), to look at the smartphone centric market transformation as an opportunity to secure or improve their market share, especially in light of the fact they should have plenty of unused radio spectrum capacities to make their offers more consumer-appealing,” the report finds. But in fact these new entrants have priced their services very closely in alignment with the larger two.

“Undoubtedly, multinational incumbent telco groups and their investors have good reasons to lobby EU decision makers to enact friendly policies that will protect their inherited oligopolistic high profit margins,” the report states. “But will the German model serve the best interest of consumers and business in other EU member states? In Rewheel’s opinion, clearly not. Enforcing an overly ‘convergent player friendly’ German model would severely limit competition in the mobile markets, leading to high prices for consumers and the Internet of mobile things and sever under-utilization of the member states’ scarce national radio spectrum resources.”

[flv width=”640″ height=”380″]http://www.phillipdampier.com/video/Bloomberg ATT Entry in Europe Not Seen as Competitive Threat 7-15-13.flv[/flv]

Competition is brutal in Europe’s wireless marketplace — a factor Bloomberg News says could temper AT&T’s planned “European Wireless Takeover.” What makes the difference between enormous profits in North America and heavy price discounting in Europe? Spectrum policy, which gives European competitors a more level playing field. Bloomberg analysts speculate AT&T will bankroll its rumored European buyouts and mergers with the enormous profits it earns from U.S. subscribers. (4 minutes)

Be Sure to Read Part One: Astroturf Overload — Broadband for America = One Giant Industry Front Group for an important introduction to what this super-sized industry front group is all about. Members of Broadband for America Red: A company or group actively engaging in anti-consumer lobbying, opposes Net Neutrality, supports Internet Overcharging, belongs to […]

Astroturf: One of the underhanded tactics increasingly being used by telecom companies is “Astroturf lobbying” – creating front groups that try to mimic true grassroots, but that are all about corporate money, not citizen power. Astroturf lobbying is hardly a new approach. Senator Lloyd Bentsen is credited with coining the term in the 1980s to […]

Hong Kong remains bullish on broadband. Despite the economic downturn, City Telecom continues to invest millions in constructing one of Hong Kong’s largest fiber optic broadband networks, providing fiber to the home connections to residents. City Telecom’s HK Broadband service relies on an all-fiber optic network, and has been dubbed “the Verizon FiOS of Hong […]

BendBroadband, a small provider serving central Oregon, breathlessly announced the imminent launch of new higher speed broadband service for its customers after completing an upgrade to DOCSIS 3. Along with the launch announcement came a new logo of a sprinting dog the company attaches its new tagline to: “We’re the local dog. We better be […]

Stop the Cap! reader Rick has been educating me about some of the new-found aggression by Shaw Communications, one of western Canada’s largest telecommunications companies, in expanding its business reach across Canada. Woe to those who get in the way. Novus Entertainment is already familiar with this story. As Stop the Cap! reported previously, Shaw […]

The Canadian Radio-television Telecommunications Commission, the Canadian equivalent of the Federal Communications Commission in Washington, may be forced to consider American broadband policy before defining Net Neutrality and its role in Canadian broadband, according to an article published today in The Globe & Mail. [FCC Chairman Julius Genachowski’s] proposal – to codify and enforce some […]

In March 2000, two cable magnates sat down for the cable industry equivalent of My Dinner With Andre. Fine wine, beautiful table linens, an exquisite meal, and a Monopoly board with pieces swapped back and forth representing hundreds of thousands of Canadian consumers. Ted Rogers and Jim Shaw drew a line on the western Ontario […]

Just like FairPoint Communications, the Towering Inferno of phone companies haunting New England, Frontier Communications is making a whole lot of promises to state regulators and consumers, if they’ll only support the deal to transfer ownership of phone service from Verizon to them. This time, Frontier is issuing a self-serving press release touting their investment […]

I see it took all of five minutes for George Ou and his friends at Digital Society to be swayed by the tunnel vision myopia of last week’s latest effort to justify Internet Overcharging schemes. Until recently, I’ve always rationalized my distain for smaller usage caps by ignoring the fact that I’m being subsidized by […]

In 2007, we took our first major trip away from western New York in 20 years and spent two weeks an hour away from Calgary, Alberta. After two weeks in Kananaskis Country, Banff, Calgary, and other spots all over southern Alberta, we came away with the Good, the Bad, and the Ugly: The Good Alberta […]

A federal appeals court in Washington has struck down, for a second time, a rulemaking by the Federal Communications Commission to limit the size of the nation’s largest cable operators to 30% of the nation’s pay television marketplace, calling the rule “arbitrary and capricious.” The 30% rule, designed to keep no single company from controlling […]

Less than half of Americans surveyed by PC Magazine report they are very satisfied with the broadband speed delivered by their Internet service provider. PC Magazine released a comprehensive study this month on speed, provider satisfaction, and consumer opinions about the state of broadband in their community. The publisher sampled more than 17,000 participants, checking […]

Subscribe

Subscribe In North America, the best prices, rebates and packages are only available to new customers while customer loyalty is rewarded with rate hikes.

In North America, the best prices, rebates and packages are only available to new customers while customer loyalty is rewarded with rate hikes.

A

A

The three companies that control 90 percent of Canada’s cell phone marketplace have set what they argue is ‘cut-throat’ competition aside to team up in a multi-million dollar lobbying campaign to discourage Verizon Wireless from entering the country.

The three companies that control 90 percent of Canada’s cell phone marketplace have set what they argue is ‘cut-throat’ competition aside to team up in a multi-million dollar lobbying campaign to discourage Verizon Wireless from entering the country. contracts until the government banned them earlier this year) and a service plan running $80 a month offering the same 500MB of data and unlimited domestic calling and texting. Rogers charges extra if customers want to text a customer outside of Canada, however.

contracts until the government banned them earlier this year) and a service plan running $80 a month offering the same 500MB of data and unlimited domestic calling and texting. Rogers charges extra if customers want to text a customer outside of Canada, however. Telus had already done its part, attempting to scoop up another scrappy upstart carrier that wanted out of the wireless business. But the Canadian government rejected Telus’ proposed acquisition of Mobilicity, claiming it would harm efforts to expand Canadian wireless competition. Not to be deterred, Rogers is now attempting a

Telus had already done its part, attempting to scoop up another scrappy upstart carrier that wanted out of the wireless business. But the Canadian government rejected Telus’ proposed acquisition of Mobilicity, claiming it would harm efforts to expand Canadian wireless competition. Not to be deterred, Rogers is now attempting a

“The U.S. government is not giving Canadian wireless carriers any special access to the U.S. market,” says a website launched by the big three cell providers to drum up support for a “level playing field.” “Then why is it that our own government is giving American companies preferential treatment over our own companies?”

“The U.S. government is not giving Canadian wireless carriers any special access to the U.S. market,” says a website launched by the big three cell providers to drum up support for a “level playing field.” “Then why is it that our own government is giving American companies preferential treatment over our own companies?” “Someone mark the date,” Tweeted one Halifax woman not inclined to vote Conservative. “Stephen Harper has done something I mostly support.”

“Someone mark the date,” Tweeted one Halifax woman not inclined to vote Conservative. “Stephen Harper has done something I mostly support.”

Analysts suspect Verizon’s interest in Canada has little to do with wooing Canadians to Big Red. Many suspect Verizon’s true interest is to make life easier for its traveling American customers who head north for business or pleasure.

Analysts suspect Verizon’s interest in Canada has little to do with wooing Canadians to Big Red. Many suspect Verizon’s true interest is to make life easier for its traveling American customers who head north for business or pleasure. In the race to acquire spectrum and market share, AT&T and Verizon Wireless have already won most of the awards worth taking and have little to fear from smaller competitors. The U.S. government has seen to that.

In the race to acquire spectrum and market share, AT&T and Verizon Wireless have already won most of the awards worth taking and have little to fear from smaller competitors. The U.S. government has seen to that.