Comcast says you must have the option to pay more for the same broadband service you already get, only now with an allowance

Comcast has announced it is considering testing an innovative new plan in several test markets offering “unlimited Internet access” to customers for a yet-to-be-determined price. Whoever heard of such a thing?

Comcast’s executive vice president David Cohen raised eyebrows last week when he predicted all Comcast customers nationwide would see usage-based billing for their Internet access within five years.

Such statements tend to muck up things like a $45 billion dollar merger with Time Warner Cable that both companies must prove is in the public interest. The buyer wants to limit your Internet usage and the seller got its fingers burned back in 2009 when it tried its own usage cap experiment and now advertises it has no data caps.

Telling Time Warner Cable customers it is in their best interest to lose unmetered Internet plans may be too tough to sell, so Cohen has spent much of this week backtracking and claiming he was “misunderstood:”

To be clear, we have no plans to announce a new data usage policy. In 2012, we suspended our 250 GB data cap in order to conduct a few pilot programs that were more customer friendly than a static cap. Since then, we’ve had no data caps for any of our customers anywhere in the country. We have been trialing a few flexible data consumption plans, including a plan that enables customers who wanted to use more data be given the option to pay more to do so, and a plan for those who use less data the option to save some money. We decided to implement these trials to learn what our customers’ reaction is to what we think are reasonable data consumption plans. We certainly have no interest in adopting any plans that our customers find unreasonable or disruptive to their Internet experience.

It’s important to note that we remain in trial mode only. We’re now also looking at adding some unlimited data plans to our trials. We have always said that as the Internet, and our customers’ use of it, continues to evolve, so will Comcast and our policies.

Cohen makes a careful distinction between a strict usage limit and the kind of usage-based billing that will fill the company’s coffers with overlimit fees. But any usage allowance is a limit of how much you can use the Internet before something bad happens — either your access is shut off or your bill explodes.

Stop the Cap! has talked with more than a dozen customers in Comcast’s test markets about their experiences with Comcast’s “data usage policy.” Although the company claims it is seeking customer reactions, it never asks whether those customers want usage limits or not, only what kind.

Giving customers “the option to pay more” is exactly the type of thinking that won Comcast the dubious distinction of being the worst company in America. No usage plan tested by Comcast actually offers savings to customers. It simply places an artificial, arbitrary usage allowance on the overpriced broadband service the company offers now.

At this point, Comcast is not offering any unlimited use trials, but we have learned the value they are likely to place on “unlimited” based on what certain customers have paid all along for that privilege. Ars Technicareports some avoided the 250GB cap by signing up for business class service. The cost? $133.79 a month for 50/10Mbps. If Google Fiber was in town, you’d pay $70 for unlimited 1,000/1,000Mbps service, and the search engine giant would still be making money.

Cohen claims nothing is set in stone, but considering Comcast’s “don’t care” attitude towards its customers, it is a safe bet they will do what is best for shareholders and ignore complaints from customers that often have nowhere else to go for 21st century broadband speeds.

Cricket has relaunched its website with a new logo and service plans as new owner AT&T merges its value-conscious Aio prepaid offering under the acquired Cricket brand name.

Targeting the credit-challenged, Cricket’s new service plans are not groundbreaking, basically copying Aio’s recent offers. Swept away are the low-cost “pay when you use” plans that only levy charges on the days you actually use the phone. Instead, Cricket is looking for a longer, committed relationship with month-long service plans and loyalty discounts:

The relaunch of Cricket will bring changes for existing customers as AT&T begins to decommission Cricket’s freestanding CDMA 3G network in March 2015 in favor of AT&T’s GSM 4G LTE service. That means customers with current Cricket phones will need to eventually switch to a newer handset, a process being made easier with $50 rebates that can make some of Cricket’s smartphones available for free. Enroll in Cricket’s rewards program, stay with them a year, make your payments on time and you will also get a $50 device credit which can be used towards an upgrade next year.

Cricket’s data plans do not carry automatic overlimit charges. Instead, your data connection is throttled to 128kbps until your billing period resets. Customers can buy an extra gigabyte of data at any time for $10.

There are several other changes that probably won’t affect the majority of Cricket customers:

There is a $5 discount for every month you are enrolled in Auto Pay to keep your phone active;

A family plan discount provides $10 off the monthly service charge of a second line, $20 off the third line, and $30 off the fourth and fifth line, for a maximum discount of $90 a month;

While you remain on your current Cricket service (on the CDMA network) you may keep paper billing. When you transition to the new Cricket (the 4G GSM network with nationwide coverage), you will no longer receive a paper bill;

Customers participating in the 5 for $100 promotion can continue with this rate plan only while on the Cricket CDMA network;

Cricket no longer offers military or friends & family discounts;

Cricket will transition out of the wireless Lifeline program. Current Lifeline customers can use Cricket’s CDMA network until it is shut down, after which they must choose a different provider;

[flv]http://www.phillipdampier.com/video/Cricket Home New Cricket Merger Info.mp4[/flv]

AT&T keeps its name and brand completely off the relaunched Cricket and Aio combined website. This introductory video explains the merger of the two wireless brands and what customers can expect. (1:44)

New York Gov. Andrew M. Cuomo has ordered the New York State Public Service to immediately start a thorough and detailed investigation into Comcast’s proposed purchase of Time Warner Cable, using new regulatory powers to reject any merger not in the “best interest” of Time Warner’s customers in New York.

“The State is taking a hands-on review of this merger to ensure that New Yorkers benefit,” Cuomo said. “The Public Service Commission’s actions will help protect consumers by demanding company commitments to strong service quality, affordability, and availability.”

New York implemented one of the nation’s strongest cable franchise laws in April that will now require the two cable operators to prove that any merger is in the public interest. An earlier law backed by the telecom industry put the burden of proof on the Commission to prove such transactions were not beneficial to the public.

Cuomo has requested the PSC check how the proposed merger will expand broadband in under-served areas and offer better broadband access to schools. The PSC will critically review the protections being offered to low income customers as well as how the proposed merger might impact consumer pricing and telecommunication competition overall.

PSC chair Audrey Zibelman said, “To determine whether the proposed transaction is in the public interest, the Commission will examine the proposal to ensure services the merged company would provide will be better than the service customers currently receive.”

One way to prove the merged company would not offer better service is to alert the Commission Comcast plans to reimpose usage caps on its customers while Time Warner Cable does not have any compulsory usage limits or usage billing.

Time Warner now serves 2.6 million subscribers in every major New York community: Buffalo, Rochester, Syracuse, Albany and the boroughs of Manhattan, Staten Island, Queens and parts of Brooklyn.

The PSC is likely to hold public forums across the state in June to hear the views of affected consumers, but the record is now open to written and telephoned comments from anyone interested in the merger.

There are several ways to provide your comments to the Commission. Comments should refer to: “Case 14-M-0183.”

Via the Internet or Mail: The public may send comments electronically to the Hon. Kathleen H. Burgess, Secretary, at [email protected] or by mail or delivery to Secretary Burgess at the New York State Public Service Commission, Three Empire State Plaza, Albany, New York 12223-1350. Comments may also be entered directly into the case file by clicking on the “Post Comments” box at the top of the page.

Toll-Free Opinion Line: Individuals may choose to phone in comments by calling the Commission’s Opinion Line at 1 800-335-2120. This line is set up to receive in-state calls 24-hours a day. These calls are not transcribed, but a summary is provided to staff who will report to the Commission.

[flv]http://www.phillipdampier.com/video/WSJ ATT Buys DirecTV 5-19-14.flv[/flv]

For $48.5 billion, AT&T will vault itself into second place among the nation’s largest pay television providers with the acquisition of DirecTV. The Wall Street Journal reports the executives at AT&T have been looking to for a giant deal for several years. Most executives earn special bonuses and other incentives worth millions for successfully completing these kinds of transactions. (3:03)

The deal, finalized on Sunday, pays $95 per DirecTV share in a combination of stock and cash, about a 10% premium over DirecTV’s closing price on Friday. Including debt, the acquisition is AT&T’s third-largest deal on record, behind the purchase of BellSouth for $83 billion in 2006 and the deal for Ameritech Corp., which closed in 1999, according to data compiled by Bloomberg.

“This is a unique opportunity that will redefine the video entertainment industry and create a company able to offer new bundles and deliver content to consumers across multiple screens – mobile devices, TVs, laptops, cars and even airplanes. At the same time, it creates immediate and long-term value for our shareholders,” said Randall Stephenson, AT&T chairman and CEO. “DirecTV is the best option for us because they have the premier brand in pay TV, the best content relationships, and a fast-growing Latin American business. DirecTV is a great fit with AT&T and together we’ll be able to enhance innovation and provide customers new competitive choices for what they want in mobile, video and broadband services. We look forward to welcoming DirecTV’s talented people to the AT&T family.”

The announced acquisition has left some on Wall Street scratching their heads.

“Like any merger born of necessity rather than opportunity, the combination of AT&T and DirecTV calls to mind images of lifeboats and rescues at sea,” telecommunications analyst Craig Moffett of MoffettNathanson Research wrote this week. AT&T, Moffett wrote, is in “dire need of a cash producer to sustain their dividend.”

[flv]http://www.phillipdampier.com/video/Bloomberg ATT DirecTV Deal a Head Scratcher 5-19-14.flv[/flv]

Craig Moffett, founder of MoffettNathanson LLC, talks about AT&T Inc.’s plan to buy DirecTV for $48.5 billion. Moffett speaks with Tom Keene, Scarlet Fu, William Cohan, and Adam Johnson on Bloomberg Television’s “Surveillance.” StockTwits founder Howard Lindzon also speaks. (5:12)

The deal would combine AT&T’s wireless, U-verse, and broadband networks with DirecTV’s television service, creating bundling opportunities for some satellite customers. As broadband becomes the most important component of a package including phone, television, and Internet access, not being able to offer broadband has left satellite TV companies at a competitive disadvantage. AT&T’s U-verse platform – a fiber to the neighborhood network – has given AT&T customers an incremental broadband speed upgrade, but not one that can necessarily compete against fiber to the home or cable broadband.

Some analysts are speculating AT&T will eventually shut down its U-verse television service and dedicate its bandwidth towards a more robust broadband offering. Existing television customers would be offered DirecTV instead.

But deal critics contend AT&T is spending a lot of money to buy its competitors instead of investing enough in network upgrades.

“The amount of cash alone AT&T is spending on this deal — $14.55 billion — is as much as it cost Verizon for its entire FiOS deployment, which reaches more than 17 million homes,” Free Press’ Derek Turner tells Stop the Cap! “Add in the $33 billion in AT&T stock and $18.6 billion in debt, and you can see just how wasteful this merger is.”

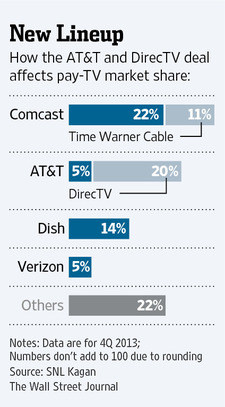

In effect, AT&T is spending nearly $50 billion to buy DirecTV’s customer relationships, its satellite platform, and its agreements with programmers, all while removing one competitor from the market. Cable has 54 percent of the pay TV market, satellite has 34 percent, and AT&T and Verizon share 11 percent. AT&T’s U-verse has 5.7 million TV customers. DirecTV has 20.3 million. Combining the two gives AT&T 26 million television customers, second only to Comcast/Time Warner Cable.

Rural Americans will effectively see their choice in competitors drop by one-third, giving them the option of the phone company or Dish Network.

AT&T intends to persuade regulators to approve the deal despite its antitrust implications by offering several commitments the company says are in the public interest and protect consumers:

15 Million Customer Locations Get More High Speed Broadband Competition. AT&T will use the merger synergies to expand its plans to build and enhance high-speed broadband service to 15 million customer locations, mostly in rural areas where AT&T does not provide high-speed broadband service today, utilizing a combination of technologies including fiber to the premises and fixed wireless local loop capabilities. This new commitment, to be completed within four years after close, is on top of the fiber and Project VIP broadband expansion plans AT&T has already announced. Customers will be able to buy broadband service stand-alone or as part of a bundle with other AT&T services.

Stand-Alone Broadband. For customers who only want a broadband service and may choose to consume video through an over-the-top (OTT) service like Netflix or Hulu, the combined company will offer stand-alone wireline broadband service at speeds of at least 6Mbps (where feasible) in areas where AT&T offers wireline IP broadband service today at guaranteed prices for three years after closing.

Nationwide Package Pricing on DIRECTV. DIRECTV’s TV service will continue to be available on a stand-alone basis at nationwide package prices that are the same for all customers, no matter where they live, for at least three years after closing.

Net Neutrality Commitment. Continued commitment for three years after closing to the FCC’s Open Internet protections established in 2010, irrespective of whether the FCC re-establishes such protections for other industry participants following the DC Circuit Court of Appeals vacating those rules.

Spectrum Auction. The transaction does not alter AT&T’s plans to meaningfully participate in the FCC’s planned spectrum auctions later this year and in 2015. AT&T intends to bid at least $9 billion in connection with the 2015 incentive auction provided there is sufficient spectrum available in the auction to provide AT&T a viable path to at least a 2×10 MHz nationwide spectrum footprint.

[flv]http://www.phillipdampier.com/video/CNN ATT DirecTV Merger 5-19-14.flv[/flv]

CNN says AT&T’s buyout of DirecTV is about getting video programming to customers using all types of technology, but public interest groups suspect it’s about reducing competition. (1:17)

A closer look at AT&T’s commitments exposes several loopholes, however.

AT&T U-verse and DirecTV compete head-on in these areas.

AT&T’s “commitment” to expand broadband to 15 million new locations is in addition to their Project VIP U-verse expansion now underway. However, AT&T does not say how many rural customers will see wired U-verse service finally become available vs. how many will lose their landlines permanently and have to rely on AT&T’s wireless landline replacement and expensive, usage-capped wireless broadband;

AT&T’s speed commitment is largely unenforceable and falls apart with language like, “where feasible.” Anywhere they don’t deliver 6Mbps DSL speed can easily be explained away as “unfeasible.” AT&T also only commits to providing DSL where it already offers DSL, so no expansion there;

The FCC’s Net Neutrality protections never covered wireless and three years is a very short time to commit to the “light touch” approach the FCC had with Net Neutrality back in 2010;

AT&T’s wireless auction commitment comes with loopholes like “meaningfully,” “provided there,” and “a viable path to at least.”

“You can’t justify AT&T buying DirecTV by pointing at Comcast’s grab for Time Warner, because neither one is a good deal for consumers,” said Delara Derakhshani, policy counsel for Consumers Union, the advocacy arm of Consumer Reports. “On the heels of Comcast’s bid for Time Warner Cable, AT&T is going to try to pull off a mega-merger of its own. These could be the start of a wave of mergers that should put federal regulators on high alert. AT&T’s takeover of DirecTV is just the latest attempt at consolidation in a marketplace where consumers are already saddled with lousy service and price hikes. The rush is on for some of the biggest industry players to get even bigger, with consumers left on the losing end.”

“The captains of our communications industry have clearly run out of ideas,” said Craig Aaron, president of Free Press. “Instead of innovating and investing in their networks, companies like AT&T and Comcast are simply buying up the competition. These takeovers are expensive, and consumers end up footing the bill for merger mania. AT&T is willing to pay $48.5 billion and take on an additional $19 billion in debt to buy DirecTV. That’s a fortune to spend on a satellite-only company at a time when the pay-TV industry is stagnating and broadband is growing. For the amount of money and debt AT&T and Comcast are collectively shelling out for their respective mega-deals, they could deploy super-fast gigabit-fiber broadband service to every single home in America.”

[flv]http://www.phillipdampier.com/video/CNN Al Franken Skeptical About DirecTV Deal 5-19-14.flv[/flv]

Sen. Al Franken (D-Minn.) appeared on CNN’s New Day this morning to express his skepticism about the consumer benefits of a merger between AT&T and DirecTV. “We need more competition, not less.” (2:40)

“Comcast Corp.’s bid to buy Time Warner Cable Inc. may be the opening act for a yearlong festival of telecommunications deals that would alter Internet, phone and TV service for tens of millions of Americans.” — Bloomberg News, May 14, 2014

Wall Street analysts remain certain Comcast and Time Warner Cable won’t be the only merger on the table this year as the $45 billion dollar deal is expected to spark a new wave of consolidation, further reducing competitive choice in telecom services for most Americans.

While the industry continues to insist that the current foundation of deregulation is key to investment and competition, the reality on the ground is less certain.

Let’s review history:

For several decades, the cable industry has avoided head-on competition with other cable operators. They argue the costs of “overbuilding” cable systems into territories already serviced by another company is financially impractical and reckless. But that did not stop telephone companies like AT&T and Verizon from overhauling portions of their networks to compete, and in at least some communities another provider has emerged to offer some competition. Some wonder if AT&T was willing to spend billions to upgrade their urban landline network to provide U-verse, why won’t cable companies spend some money and compete directly with one another?

The answer is simple: They can earn a lot more by limiting competition.

When only a few firms account for most of the sales of a product, those firms can sometimes exercise market power by either explicitly or implicitly coordinating their actions. Coordinated interaction is especially suspect where all firms seem to charge very similar prices and few, if any, are willing to challenge the status quo.

Since the 1980s, the telecommunications industry has been deregulated off and on to a degree not seen since the pioneer days of telephone service. That was the era when waves of mergers created near-monopolies in the oil, railroad, energy, tobacco, steel and sugar industries. By the late 1890s, evidence piled up that proved reducing the number of providers in a market leads to higher prices and poor service. The abuses eventually led to the passage of the Sherman Antitrust Act of 1890 and later the Clayton Antitrust Act of 1914.

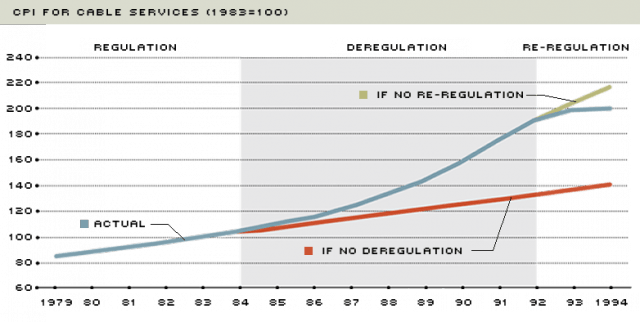

Here is what happened when the cable industry was reined in during the early 1990s, only to be deregulated again.

The generation of political leaders that dominated Washington during the 1980s developed selective amnesia about economic history and dismantled many of the regulatory protections established to protect consumers, arguing competition would keep markets in check. In the broadband and cable business, that has not proved as successful as the industry represents.

At the heart of the problem is the 1996 Telecommunications Act, signed into law by President Bill Clinton. The sweeping law is littered with lobbyist landmines for consumers and their interests. Under the guise of increasing competition, the 1996 law actually helped reduce competition by removing regulatory oversight and, perhaps unintentionally, sparking an enormous rampage of industry consolidation followed by price increases. The Bush Administration kept the war on consumers going with the appointment of Michael Powell (now the CEO of the cable industry’s lobbying group) to chair the Federal Communications Commission. Under Powell, non-discriminatory access to networks by competitors was curtailed, and Powell’s FCC gave carte blanche to the cable industry’s plan to cluster its territories into large regional monopolies and a tight national oligopoly. The FCC’s own researchers quietly admitted in the early 2000s “clustering raised prices.”

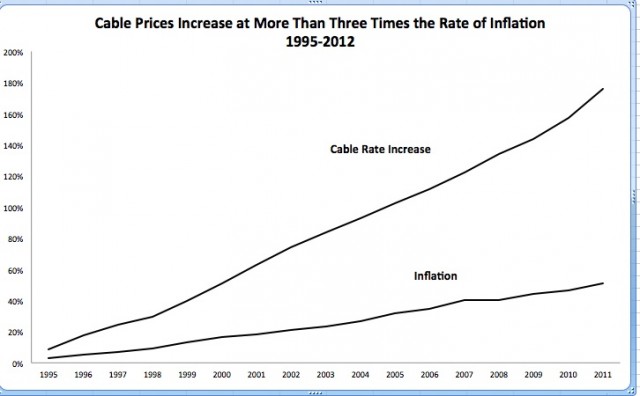

By January 2001, cable operators had settled on rate increases that averaged three times the rate of inflation. While the national inflation rate hovered around 1%, cable companies routinely raised basic cable rates an average of 7% annually. Powell declared rising cable rates were not a consumer problem and adopted the industry’s classic talking point that rate increases reflect the “value of the programming” found on cable. In fact, even as cable customers grew increasingly angry about rate increases, Powell told three different reporters he wanted to further relax the FCC’s involvement in cable pricing. (McClintock, Pamela, “Powell: No Cable Coin Crisis” Variety, April 30, 2001; Hearn, Ted. “Powell: Value Matters in Cable Rates,” Multichannel News, March 13, 2002; Powell Press Conference, February 8, 2001; Dreazen, Yochi. “FCC Chairman Signals Change, Plans to Limit Intervention,” Wall Street Journal, February 7, 2001.)

Economists reviewing data found in publicly available corporate balance sheets soon found evidence that the “increased programming costs”-excuse for rate increases did not hold water. The less competition or number of choices available to consumers in the market unambiguously lead to higher prices. It has remained true since Consumers’ Union revealed the financial trickery in 2003:

The cable industry will claim that programming costs are driving prices up. While programming costs have certainly risen, a close look at the numbers shows that rising program costs account for only a small part of the rising rates.

If costs were really the cause of rising prices, then the cable industries’ operating margins – the difference between its revenues and costs — would not be rising. The facts are just the opposite. Operating margins have been increasing dramatically since 1997. The operating margin for the industry as a whole will reach $18.8 billion per year in 2002, $7 billion more than it was in 1997. Operating revenues per subscriber have increased dramatically over that period, from $208 per year to $273. That is, after taking out all the operating costs, including programming costs, cable operators have increased their take per subscriber by over 30 percent.

[…] The ability of cable operators to raise rates and increase revenues, even with rising programming costs, stems from the market power they have at the point of sale. They would not be able to raise prices and pass program price increases through if they did not have monopoly power.

Consumers’ Union also foreshadows what will happen if another wave of industry consolidation takes hold the way it did over a decade earlier:

While the cable industry has certainly increased capital expenditures to upgrade its plants, it has actually sunk a lot more capital into another activity – mergers and acquisitions.

It is the outrageous prices that have been paid to buy each other out and consolidate the industry that is helping to drive the rate increases. Between 1998, when the first mega merger between cable operators was announced, and 2001, when the last big merger was announced, cable companies spent over a quarter of a trillion dollars buying each other out. In those four years, they spent almost six times as much on mergers and acquisitions as they did on capital expenditures to upgrade their systems. At the same time, the average price paid per subscriber more than doubled.

When a cable operator pays such an outrageous price, the previous owner is reaping the financial rewards of his monopoly power. The acquiring company can only pay such a high price by assuming that his monopoly power will allow him to continue to increase prices. Monopoly power is being bought and sold and borrowed against. The new cable operator, who has paid for market power, may insist that the debt he has incurred to obtain it is a real cost on his books. That may be correct in the literal sense (he owes someone that money) but that does not make it right, or the abuse of market power legal.

“My concern is the merger and the consolidation of the cable and internet delivery system for consumers and what will happen to internet and cable rates and choices,” Maxcy said, voicing his hesitancy about a deal that merges the nation’s two largest cable providers. “As that industry has gotten more consolidated over time, we have seen rates go up. The answer from them is that we’ve got more choices. Are we better off or not better off? I don’t know, but certainly rates have gone up at a much faster rate than the inflation rate. The result of more monopoly power is always higher prices and less choices and it seems that this merger moves in that direction.”

“The threat from non-network content providers is a concern for the cable industry,” Maxcy added.

“We’re moving to a situation where we don’t need cable, but we still need the internet and the cable companies are the ones that have control of that,” he said. “Consolidating them together makes them more competitive against the outside forces, but the other argument makes the whole thing less competitive so they’ll have more ability to control the access to Netflix, YouTube and the like. People that may develop other similar sorts of services will have a hard time getting the access they would like to purchase those.”

Chris Stigall spoke with economist and Temple professor Joel Maxcy on Talk Radio 1210 WPHT in Philadelphia about Comcast’s attempt to purchase Time Warner Cable and what that means for consumers. Feb. 18, 2014 (12:10)

You must remain on this page to hear the clip, or you can download the clip and listen later.

Be Sure to Read Part One: Astroturf Overload — Broadband for America = One Giant Industry Front Group for an important introduction to what this super-sized industry front group is all about. Members of Broadband for America Red: A company or group actively engaging in anti-consumer lobbying, opposes Net Neutrality, supports Internet Overcharging, belongs to […]

Astroturf: One of the underhanded tactics increasingly being used by telecom companies is “Astroturf lobbying” – creating front groups that try to mimic true grassroots, but that are all about corporate money, not citizen power. Astroturf lobbying is hardly a new approach. Senator Lloyd Bentsen is credited with coining the term in the 1980s to […]

Hong Kong remains bullish on broadband. Despite the economic downturn, City Telecom continues to invest millions in constructing one of Hong Kong’s largest fiber optic broadband networks, providing fiber to the home connections to residents. City Telecom’s HK Broadband service relies on an all-fiber optic network, and has been dubbed “the Verizon FiOS of Hong […]

BendBroadband, a small provider serving central Oregon, breathlessly announced the imminent launch of new higher speed broadband service for its customers after completing an upgrade to DOCSIS 3. Along with the launch announcement came a new logo of a sprinting dog the company attaches its new tagline to: “We’re the local dog. We better be […]

Stop the Cap! reader Rick has been educating me about some of the new-found aggression by Shaw Communications, one of western Canada’s largest telecommunications companies, in expanding its business reach across Canada. Woe to those who get in the way. Novus Entertainment is already familiar with this story. As Stop the Cap! reported previously, Shaw […]

The Canadian Radio-television Telecommunications Commission, the Canadian equivalent of the Federal Communications Commission in Washington, may be forced to consider American broadband policy before defining Net Neutrality and its role in Canadian broadband, according to an article published today in The Globe & Mail. [FCC Chairman Julius Genachowski’s] proposal – to codify and enforce some […]

In March 2000, two cable magnates sat down for the cable industry equivalent of My Dinner With Andre. Fine wine, beautiful table linens, an exquisite meal, and a Monopoly board with pieces swapped back and forth representing hundreds of thousands of Canadian consumers. Ted Rogers and Jim Shaw drew a line on the western Ontario […]

Just like FairPoint Communications, the Towering Inferno of phone companies haunting New England, Frontier Communications is making a whole lot of promises to state regulators and consumers, if they’ll only support the deal to transfer ownership of phone service from Verizon to them. This time, Frontier is issuing a self-serving press release touting their investment […]

I see it took all of five minutes for George Ou and his friends at Digital Society to be swayed by the tunnel vision myopia of last week’s latest effort to justify Internet Overcharging schemes. Until recently, I’ve always rationalized my distain for smaller usage caps by ignoring the fact that I’m being subsidized by […]

In 2007, we took our first major trip away from western New York in 20 years and spent two weeks an hour away from Calgary, Alberta. After two weeks in Kananaskis Country, Banff, Calgary, and other spots all over southern Alberta, we came away with the Good, the Bad, and the Ugly: The Good Alberta […]

A federal appeals court in Washington has struck down, for a second time, a rulemaking by the Federal Communications Commission to limit the size of the nation’s largest cable operators to 30% of the nation’s pay television marketplace, calling the rule “arbitrary and capricious.” The 30% rule, designed to keep no single company from controlling […]

Less than half of Americans surveyed by PC Magazine report they are very satisfied with the broadband speed delivered by their Internet service provider. PC Magazine released a comprehensive study this month on speed, provider satisfaction, and consumer opinions about the state of broadband in their community. The publisher sampled more than 17,000 participants, checking […]

Subscribe

Subscribe

Stop the Cap! has talked with more than a dozen customers in Comcast’s test markets about their experiences with Comcast’s “data usage policy.” Although the company claims it is seeking customer reactions, it never asks whether those customers want usage limits or not, only what kind.

Stop the Cap! has talked with more than a dozen customers in Comcast’s test markets about their experiences with Comcast’s “data usage policy.” Although the company claims it is seeking customer reactions, it never asks whether those customers want usage limits or not, only what kind.

One way to prove the merged company would not offer better service is to alert the Commission Comcast plans to reimpose usage caps on its customers while Time Warner Cable does not have any compulsory usage limits or usage billing.

One way to prove the merged company would not offer better service is to alert the Commission Comcast plans to reimpose usage caps on its customers while Time Warner Cable does not have any compulsory usage limits or usage billing. The deal, finalized on Sunday, pays $95 per DirecTV share in a combination of stock and cash, about a 10% premium over DirecTV’s closing price on Friday. Including debt, the acquisition is AT&T’s third-largest deal on record, behind the purchase of BellSouth for $83 billion in 2006 and the deal for Ameritech Corp., which closed in 1999, according to data compiled by Bloomberg.

The deal, finalized on Sunday, pays $95 per DirecTV share in a combination of stock and cash, about a 10% premium over DirecTV’s closing price on Friday. Including debt, the acquisition is AT&T’s third-largest deal on record, behind the purchase of BellSouth for $83 billion in 2006 and the deal for Ameritech Corp., which closed in 1999, according to data compiled by Bloomberg. The deal would combine AT&T’s wireless, U-verse, and broadband networks with DirecTV’s television service, creating bundling opportunities for some satellite customers. As broadband becomes the most important component of a package including phone, television, and Internet access, not being able to offer broadband has left satellite TV companies at a competitive disadvantage. AT&T’s U-verse platform – a fiber to the neighborhood network – has given AT&T customers an incremental broadband speed upgrade, but not one that can necessarily compete against fiber to the home or cable broadband.

The deal would combine AT&T’s wireless, U-verse, and broadband networks with DirecTV’s television service, creating bundling opportunities for some satellite customers. As broadband becomes the most important component of a package including phone, television, and Internet access, not being able to offer broadband has left satellite TV companies at a competitive disadvantage. AT&T’s U-verse platform – a fiber to the neighborhood network – has given AT&T customers an incremental broadband speed upgrade, but not one that can necessarily compete against fiber to the home or cable broadband.

“Comcast Corp.’s bid to buy Time Warner Cable Inc. may be the opening act for a yearlong festival of telecommunications deals that would alter Internet, phone and TV service for tens of millions of Americans.” — Bloomberg News, May 14, 2014

“Comcast Corp.’s bid to buy Time Warner Cable Inc. may be the opening act for a yearlong festival of telecommunications deals that would alter Internet, phone and TV service for tens of millions of Americans.” — Bloomberg News, May 14, 2014

Economists reviewing data found in publicly available corporate balance sheets soon found evidence that the “increased programming costs”-excuse for rate increases did not hold water. The less competition or number of choices available to consumers in the market unambiguously lead to higher prices. It has remained true since Consumers’ Union

Economists reviewing data found in publicly available corporate balance sheets soon found evidence that the “increased programming costs”-excuse for rate increases did not hold water. The less competition or number of choices available to consumers in the market unambiguously lead to higher prices. It has remained true since Consumers’ Union  When a cable operator pays such an outrageous price, the previous owner is reaping the financial rewards of his monopoly power. The acquiring company can only pay such a high price by assuming that his monopoly power will allow him to continue to increase prices. Monopoly power is being bought and sold and borrowed against. The new cable operator, who has paid for market power, may insist that the debt he has incurred to obtain it is a real cost on his books. That may be correct in the literal sense (he owes someone that money) but that does not make it right, or the abuse of market power legal.

When a cable operator pays such an outrageous price, the previous owner is reaping the financial rewards of his monopoly power. The acquiring company can only pay such a high price by assuming that his monopoly power will allow him to continue to increase prices. Monopoly power is being bought and sold and borrowed against. The new cable operator, who has paid for market power, may insist that the debt he has incurred to obtain it is a real cost on his books. That may be correct in the literal sense (he owes someone that money) but that does not make it right, or the abuse of market power legal.