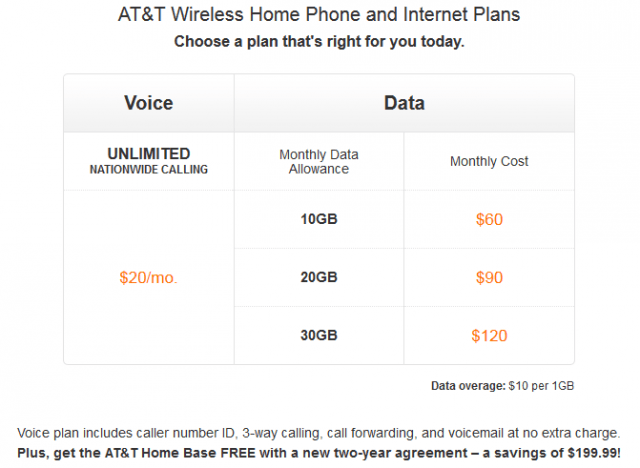

AT&T’s solution for rural Americans without access to broadband service arrived this week with the introduction of an $80/month plan bundling a mandatory wireless home landline with a 10GB usage-capped Internet plan.

AT&T Wireless Home Phone and Internet has undergone market testing in selected northeastern areas (largely outside of AT&T’s landline service territory). This week the service became available nationwide and is marketed to customers disconnected (or soon will be if regulators approve) from AT&T’s traditional landline service. AT&T is petitioning to dismantle its rural and outer suburban wired landline network and transfer customers to wireless service. But AT&T’s wireless replacement is both expensive and usage capped with an allowance that is just a fraction of what AT&T DSL offers:

Customers start with a $20/month wireless landline phone replacement, powered by AT&T’s wireless network. Customers will keep their current phone number and home phones and will be sent a “Home Base” device that will interface between AT&T’s wireless network and up to two telephones. AT&T does not permit its device to be connected to your existing home phone wiring, so it strongly urges customers to buy cordless phones. The device is portable so it can be taken with you when traveling. The standalone service offers unlimited nationwide calling, Voicemail, caller ID and call waiting;

Those interested in also purchasing broadband can add one of three different data plans: $60 for 10GB, $90 for 20GB and $120 for 30GB. AT&T charges a $10 overlimit fee for each extra gigabyte. You cannot buy broadband service unless you also subscribe to AT&T’s wireless landline product. That means the lowest possible price for rural broadband is $80 a month for up to 10GB of usage. Access may be over AT&T’s 4G LTE network (5-12Mbps maximum speeds) or their much-slower, but more common 3G network. In contrast, AT&T sells DSL for as little as $15 a month with a 150GB usage allowance included.

[flv]http://www.phillipdampier.com/video/ATT Wireless Home Phone Internet Intro 5-2014.flv[/flv]

AT&T introduces its new solution for rural America — wireless home phone and Internet service, at a price much higher than what urban customers pay. (1:42)

AT&T’s Home Base

AT&T’s Wireless Home Phone and Internet includes plenty of fine print and disclaimers:

A two-year service commitment is required to avoid a $199 charge for the Home Base device;

911 service is not guaranteed and you will be required to give your physical location to the 911 operator so they can send help to the proper address;

A backup battery powers the Home Base allowing up to 1.5 hours of talk time and 18 hours of standby time. However, a standard corded phone that does not need electric power to operate is required to place or receive calls (including 911) during a power outage;

Not compatible with wireless messaging services/text messaging, home security systems, fax machines, medical alert & monitoring systems, credit card machines, IP/PBX Phone systems, or dial-up Internet service. May not be compatible with DVR/Satellite systems;

Call quality, wireless coverage, and service reliability are not guaranteed;

Well-qualified credit approval required;

An activation fee (undisclosed) also applies.

There are many surcharges that also may apply, including a $35 restocking fee, federal, state, and local taxes and the universal service fee. Customers must also pay AT&T-originated fees kept by AT&T, including a $1.25 “cost recovery charge,” a gross receipts surcharge, administrative fees and any government-originated assessments that AT&T passes on to customers in various states.

[flv]http://www.phillipdampier.com/video/ATT Wireless Home Phone Internet Setup 5-2014.flv[/flv]

AT&T explains how to set up and configure its Home Base to receive phone and broadband service wirelessly. (3:16)

Frontier is introducing a new $5 a month disaster landline service in June.

With plenty of talk about the impact of global climate change, Frontier Communications will soon introduce a new inexpensive landline service to help customers plagued by weather disasters.

Frontier Security Phone is a $5 a month landline that can only reach 411 and 911 — perfect for those who lose their Voice over IP phone service in a power failure or find cell service clogged or otherwise unavailable.

“Our [service areas] are very prone to severe weather, lots of hurricanes, tornadoes and the mud slides in Washington State,” said Frontier CEO Maggie Wilderotter. “We have markets that are very plagued by bad weather and having a landline phone that works when your power goes out where we have a density of 34 homes a mile is important.”

Frontier will market the bare bones landline service to customers planning to disconnect service in favor of another provider as well as those that already have. Unlike basic budget service, Frontier Security Phone will not be able to make or receive regular phone calls — it is intended for emergency-use only.

Little known to most Frontier customers (and only mentioned on their website in a thicket of tariff filings) is that different types of landline service are available. By switching away from flat rate service to a measured-rate plan, where each local outgoing call is charged at a prevailing per-call rate (usually under 10 cents), customers can still have the option of making and receiving calls on a budget, especially considering incoming calls are free. In large cities like Rochester, Frontier charges $18.03 a month for flat rate local calling. If one switched to a measured-rate plan, the charge is $12.07 a month. Those interested will have to call Frontier at 1-800-921-8101 and specifically inquire about measured rate local telephone service.

Frontier is also exploring a market trial of a new Voice over IP landline service sold as a bundle with DSL.

Wilderotter told investors attending the JPMorgan Global Technology, Media and Telecom Conference that Frontier believes streaming, on-demand video is the future of Frontier, not traditional linear/live television.

Wilderotter

Therefore, despite the fact Frontier will continue to support legacy FiOS TV services in adopted Verizon markets in Indiana and the Pacific Northwest, and will likely take ownership of AT&T U-verse in Connecticut, the company has no plans to introduce cable-TV service anywhere else. The biggest reason is the cost of video programming for smaller competitors like Frontier.

“We’re never to going to be big like some of these big guys are, which is why we have a partnership with the Dish Network, because they’re big,” Wilderotter explained. “They go negotiate all the content deals and then we offer those packages to our customers and we get paid a sales commission and a monthly customer service and billing fee from Dish on behalf of that service.”

Although Frontier applauded AT&T for its announced intention to acquire DirecTV, Frontier customers in Connecticut currently subscribed to DirecTV through AT&T will eventually be switched to Dish Network — Frontier’s chosen video partner.

Wilderotter explained that Frontier can leverage its broadband network to support streaming video services without assuming the costs of licensing the content. As Comcast and AT&T grow larger, they can negotiate better volume discounts unheard of among smaller competitors, keeping companies like Frontier at a major cost disadvantage. But if a customer wants Netflix or YouTube, they will need a broadband connection to get it, which is where Frontier comes in.

“If you think about Frontier, we’re in 27 states today, soon to be 28 with the Connecticut acquisition, about 30,000 communities, predominantly rural and suburban. That’s sort of our footprint,” said Wilderotter. “So when we think strategically about the assets that we have as a company, first and foremost is [the] networks in all of those markets, and those networks have been upgraded. So for us, the cost of adding another customer to broadband is really the upfront sales cost, because the network is already in place and the capabilities are already [there].”

Wilderotter adds Frontier’s average payback on its investment to hook up a new broadband customer is about three months.

“We also have industry-leading margins in our company,” Wilderotter said. “Our margins are in the mid-40% range and we’ve typically always had very strong margins in terms of how we run the business from an efficiency and effective perspective.”

Wilderotter also told investors that Frontier plans to add several additional services powered by its broadband network over the course of this year.

“We’re really looking in the categories of home automation, security, lifestyle products and monitoring products,” Wilderotter said. “And with that, there is ongoing monthly recurring revenue in terms of the tech support that we put with that product set when we sell it to a customer.”

When Wilderotter was asked about recent price hikes implemented by Frontier, she admitted the primary reason for the increase was the lack of competitive cable pricing in the market.

“If you look at what cable is offering in our markets, they offer a standalone broadband product somewhere $35 and $65,” she said. “And that doesn’t include the modem. So we felt we could increase the price, still be very competitive in the marketplace and have a product set that made more sense for our customers at a convenient price.”

“Comcast Corp.’s bid to buy Time Warner Cable Inc. may be the opening act for a yearlong festival of telecommunications deals that would alter Internet, phone and TV service for tens of millions of Americans.” — Bloomberg News, May 14, 2014

Wall Street analysts remain certain Comcast and Time Warner Cable won’t be the only merger on the table this year as the $45 billion dollar deal is expected to spark a new wave of consolidation, further reducing competitive choice in telecom services for most Americans.

While the industry continues to insist that the current foundation of deregulation is key to investment and competition, the reality on the ground is less certain.

Let’s review history:

For several decades, the cable industry has avoided head-on competition with other cable operators. They argue the costs of “overbuilding” cable systems into territories already serviced by another company is financially impractical and reckless. But that did not stop telephone companies like AT&T and Verizon from overhauling portions of their networks to compete, and in at least some communities another provider has emerged to offer some competition. Some wonder if AT&T was willing to spend billions to upgrade their urban landline network to provide U-verse, why won’t cable companies spend some money and compete directly with one another?

The answer is simple: They can earn a lot more by limiting competition.

When only a few firms account for most of the sales of a product, those firms can sometimes exercise market power by either explicitly or implicitly coordinating their actions. Coordinated interaction is especially suspect where all firms seem to charge very similar prices and few, if any, are willing to challenge the status quo.

Since the 1980s, the telecommunications industry has been deregulated off and on to a degree not seen since the pioneer days of telephone service. That was the era when waves of mergers created near-monopolies in the oil, railroad, energy, tobacco, steel and sugar industries. By the late 1890s, evidence piled up that proved reducing the number of providers in a market leads to higher prices and poor service. The abuses eventually led to the passage of the Sherman Antitrust Act of 1890 and later the Clayton Antitrust Act of 1914.

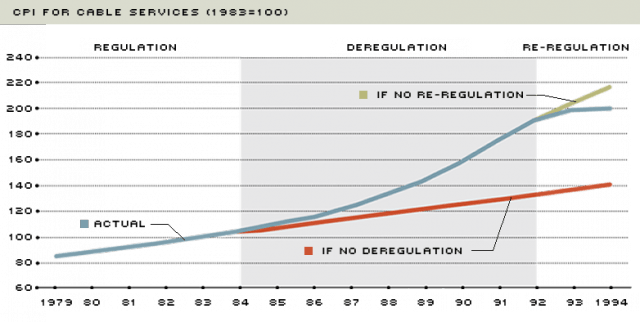

Here is what happened when the cable industry was reined in during the early 1990s, only to be deregulated again.

The generation of political leaders that dominated Washington during the 1980s developed selective amnesia about economic history and dismantled many of the regulatory protections established to protect consumers, arguing competition would keep markets in check. In the broadband and cable business, that has not proved as successful as the industry represents.

At the heart of the problem is the 1996 Telecommunications Act, signed into law by President Bill Clinton. The sweeping law is littered with lobbyist landmines for consumers and their interests. Under the guise of increasing competition, the 1996 law actually helped reduce competition by removing regulatory oversight and, perhaps unintentionally, sparking an enormous rampage of industry consolidation followed by price increases. The Bush Administration kept the war on consumers going with the appointment of Michael Powell (now the CEO of the cable industry’s lobbying group) to chair the Federal Communications Commission. Under Powell, non-discriminatory access to networks by competitors was curtailed, and Powell’s FCC gave carte blanche to the cable industry’s plan to cluster its territories into large regional monopolies and a tight national oligopoly. The FCC’s own researchers quietly admitted in the early 2000s “clustering raised prices.”

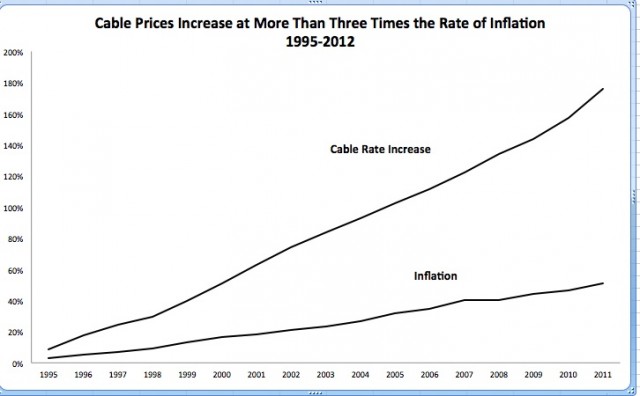

By January 2001, cable operators had settled on rate increases that averaged three times the rate of inflation. While the national inflation rate hovered around 1%, cable companies routinely raised basic cable rates an average of 7% annually. Powell declared rising cable rates were not a consumer problem and adopted the industry’s classic talking point that rate increases reflect the “value of the programming” found on cable. In fact, even as cable customers grew increasingly angry about rate increases, Powell told three different reporters he wanted to further relax the FCC’s involvement in cable pricing. (McClintock, Pamela, “Powell: No Cable Coin Crisis” Variety, April 30, 2001; Hearn, Ted. “Powell: Value Matters in Cable Rates,” Multichannel News, March 13, 2002; Powell Press Conference, February 8, 2001; Dreazen, Yochi. “FCC Chairman Signals Change, Plans to Limit Intervention,” Wall Street Journal, February 7, 2001.)

Economists reviewing data found in publicly available corporate balance sheets soon found evidence that the “increased programming costs”-excuse for rate increases did not hold water. The less competition or number of choices available to consumers in the market unambiguously lead to higher prices. It has remained true since Consumers’ Union revealed the financial trickery in 2003:

The cable industry will claim that programming costs are driving prices up. While programming costs have certainly risen, a close look at the numbers shows that rising program costs account for only a small part of the rising rates.

If costs were really the cause of rising prices, then the cable industries’ operating margins – the difference between its revenues and costs — would not be rising. The facts are just the opposite. Operating margins have been increasing dramatically since 1997. The operating margin for the industry as a whole will reach $18.8 billion per year in 2002, $7 billion more than it was in 1997. Operating revenues per subscriber have increased dramatically over that period, from $208 per year to $273. That is, after taking out all the operating costs, including programming costs, cable operators have increased their take per subscriber by over 30 percent.

[…] The ability of cable operators to raise rates and increase revenues, even with rising programming costs, stems from the market power they have at the point of sale. They would not be able to raise prices and pass program price increases through if they did not have monopoly power.

Consumers’ Union also foreshadows what will happen if another wave of industry consolidation takes hold the way it did over a decade earlier:

While the cable industry has certainly increased capital expenditures to upgrade its plants, it has actually sunk a lot more capital into another activity – mergers and acquisitions.

It is the outrageous prices that have been paid to buy each other out and consolidate the industry that is helping to drive the rate increases. Between 1998, when the first mega merger between cable operators was announced, and 2001, when the last big merger was announced, cable companies spent over a quarter of a trillion dollars buying each other out. In those four years, they spent almost six times as much on mergers and acquisitions as they did on capital expenditures to upgrade their systems. At the same time, the average price paid per subscriber more than doubled.

When a cable operator pays such an outrageous price, the previous owner is reaping the financial rewards of his monopoly power. The acquiring company can only pay such a high price by assuming that his monopoly power will allow him to continue to increase prices. Monopoly power is being bought and sold and borrowed against. The new cable operator, who has paid for market power, may insist that the debt he has incurred to obtain it is a real cost on his books. That may be correct in the literal sense (he owes someone that money) but that does not make it right, or the abuse of market power legal.

“My concern is the merger and the consolidation of the cable and internet delivery system for consumers and what will happen to internet and cable rates and choices,” Maxcy said, voicing his hesitancy about a deal that merges the nation’s two largest cable providers. “As that industry has gotten more consolidated over time, we have seen rates go up. The answer from them is that we’ve got more choices. Are we better off or not better off? I don’t know, but certainly rates have gone up at a much faster rate than the inflation rate. The result of more monopoly power is always higher prices and less choices and it seems that this merger moves in that direction.”

“The threat from non-network content providers is a concern for the cable industry,” Maxcy added.

“We’re moving to a situation where we don’t need cable, but we still need the internet and the cable companies are the ones that have control of that,” he said. “Consolidating them together makes them more competitive against the outside forces, but the other argument makes the whole thing less competitive so they’ll have more ability to control the access to Netflix, YouTube and the like. People that may develop other similar sorts of services will have a hard time getting the access they would like to purchase those.”

Chris Stigall spoke with economist and Temple professor Joel Maxcy on Talk Radio 1210 WPHT in Philadelphia about Comcast’s attempt to purchase Time Warner Cable and what that means for consumers. Feb. 18, 2014 (12:10)

You must remain on this page to hear the clip, or you can download the clip and listen later.

Verizon’s FiOS expansion is still as dead as Francisco Franco.

Verizon is prepared to watch up to 30% of their copper landline customers drift away because the company is adamant about no further expansion of its FiOS fiber to the home network.

Fran Shammo, chief financial officer at Verizon, told attendees of the Jefferies Global Technology, Media & Telecom Conference that Verizon will complete the buildout of its fiber network to a total of about 19 million homes, and that is it.

“Look, we will continue to fulfill our FiOS license franchise agreements,” Frammo said. “[We will] cover about 70% of our legacy footprint. So 30%, we are not going to cover. That is where we are still going to have copper.”

That is bad news for Verizon customers stuck with the company’s copper network because Verizon isn’t planning any further significant investments in it.

“We will continue to harvest that copper network and those customers and keep them as long as we can,” Frammo said. “But we will not be building FiOS out for those areas.”

In fact, Frammo admitted ongoing cost-cutting at Verizon’s landline division is allowing the company to shift more money and resources to its more profitable wireless network.

Verizon CEO Lowell McAdam doesn’t want to spend money on non-FiOS areas when more can be made from its wireless network.

“It is also taking cost structure out,” Frammo said. “As I mentioned, the migration of copper to fiber has been very big for us. Our Lean Six Sigma projects have really significantly helped us in our capital investment in the wireline which is why I can put more money into the wireless side of the business.”

Verizon has shifted an increasing proportion of its capital investments towards its wireless division year after year, while cutting ongoing investment in wireline. Ratepayers are not benefiting from this arrangement, and critics contend Verizon landline customers are effectively subsidizing Verizon’s wireless networks.

Verizon will still complete the FiOS buildouts it committed to earlier, particularly in New York City, but it is increasingly unlikely Verizon will ever start another wave of fiber upgrades.

In fact, Michael McCormack, the Jefferies’ Wall Street analyst questioning Shammo at the conference foreshadowed what is more likely to happen to Verizon’s legacy copper customers.

“We have talked extensively in the past about the non-FiOS areas and I guess in my second reincarnation as a banker, I will try to help you get rid of those assets,” said McCormack.

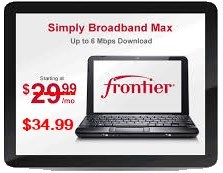

As of May 1st, Frontier Communications has raised the price of its standalone DSL service $5 a month, primarily because its competitors have also raised prices.

Current subscribers to Frontier’s basic 6Mbps ADSL service Simply Broadband will continue to pay $29.99 a month for now, but new customers will see a rate increase to $34.99.

“We increased the price [… because it] better reflects the value of that offering, given the robust capability of our network and comparable pricing from our competitors,” Frontier CEO Maggie Wilderotter told Wall Street analysts on a quarterly results conference call.

Frontier also announced Frontier FiOS TV price increases that “reflect increasing programming costs” also taking effect this month.

Frontier added 37,000 new broadband customers during the first quarter, a record for the company and the fifth consecutive quarter of broadband customer growth. Frontier increasingly depends on broadband to retain existing customers and develop new customer relationships in rural areas where broadband service has not been available in the past.

“As of April, 74% of our customers have access to 12Mbps, up from 60% in the fourth quarter,” said chief operating officer Dan McCarthy. “Now 61% of households we pass can get 20Mbps or greater, and 83% can get 6Mbps. At the end of the fourth quarter in 2012 only 40% of our network was capable of 20Mbps and only 50% was capable of 12Mbps.”

Despite the speed increases, cable competitors still made their presence known. Most cable companies sell faster service than Frontier offers and on the low-end, Time Warner Cable’s 2Mbps $15 broadband package, marketed to current DSL customers, was acknowledged to have an impact by Wilderotter, but not enough to bring a significant change in competitive intensity.

Frontier continues to argue that broadband speeds are simply not that important to most customers. McCarthy claimed that less than 20% of Frontier’s broadband customers subscribe to speeds above 6Mbps.

“Quite frankly we’ve had focus groups with our customers and potential customers […] and what they say is that they don’t really know what speed they have,” McCarthy said. “They just need enough and that’s really what it’s about — providing a good quality product that’s reliable and gives them the speed that they need. It’s not necessarily a 60Mbps connection that they’re really never going to use.”

“We’ve also found [in the focus groups that we do] that a lot of customers, even those upgrading to higher speeds don’t really change their behavior,” Wilderotter added. “It’s not like they have 10Mbps more so now they’re a gamer. They just keep doing the same thing they were doing before. We still have the majority of our customers taking around 6Mbps and they have a choice to go up but they decide that that’s enough for what they’re doing and we’re happy to sell them just what they need.”

Frontier has also reduced its landline losses nationwide to 9,600 during the last quarter. It will begin running advertising this year that reminds customers landline service is often more robust than wireless or Voice over IP during power or weather-related outages. Wilderotter said emphasizing the traditional landline as a protective and security measure really resonates with Frontier’s customers.

Be Sure to Read Part One: Astroturf Overload — Broadband for America = One Giant Industry Front Group for an important introduction to what this super-sized industry front group is all about. Members of Broadband for America Red: A company or group actively engaging in anti-consumer lobbying, opposes Net Neutrality, supports Internet Overcharging, belongs to […]

Astroturf: One of the underhanded tactics increasingly being used by telecom companies is “Astroturf lobbying” – creating front groups that try to mimic true grassroots, but that are all about corporate money, not citizen power. Astroturf lobbying is hardly a new approach. Senator Lloyd Bentsen is credited with coining the term in the 1980s to […]

Hong Kong remains bullish on broadband. Despite the economic downturn, City Telecom continues to invest millions in constructing one of Hong Kong’s largest fiber optic broadband networks, providing fiber to the home connections to residents. City Telecom’s HK Broadband service relies on an all-fiber optic network, and has been dubbed “the Verizon FiOS of Hong […]

BendBroadband, a small provider serving central Oregon, breathlessly announced the imminent launch of new higher speed broadband service for its customers after completing an upgrade to DOCSIS 3. Along with the launch announcement came a new logo of a sprinting dog the company attaches its new tagline to: “We’re the local dog. We better be […]

Stop the Cap! reader Rick has been educating me about some of the new-found aggression by Shaw Communications, one of western Canada’s largest telecommunications companies, in expanding its business reach across Canada. Woe to those who get in the way. Novus Entertainment is already familiar with this story. As Stop the Cap! reported previously, Shaw […]

The Canadian Radio-television Telecommunications Commission, the Canadian equivalent of the Federal Communications Commission in Washington, may be forced to consider American broadband policy before defining Net Neutrality and its role in Canadian broadband, according to an article published today in The Globe & Mail. [FCC Chairman Julius Genachowski’s] proposal – to codify and enforce some […]

In March 2000, two cable magnates sat down for the cable industry equivalent of My Dinner With Andre. Fine wine, beautiful table linens, an exquisite meal, and a Monopoly board with pieces swapped back and forth representing hundreds of thousands of Canadian consumers. Ted Rogers and Jim Shaw drew a line on the western Ontario […]

Just like FairPoint Communications, the Towering Inferno of phone companies haunting New England, Frontier Communications is making a whole lot of promises to state regulators and consumers, if they’ll only support the deal to transfer ownership of phone service from Verizon to them. This time, Frontier is issuing a self-serving press release touting their investment […]

I see it took all of five minutes for George Ou and his friends at Digital Society to be swayed by the tunnel vision myopia of last week’s latest effort to justify Internet Overcharging schemes. Until recently, I’ve always rationalized my distain for smaller usage caps by ignoring the fact that I’m being subsidized by […]

In 2007, we took our first major trip away from western New York in 20 years and spent two weeks an hour away from Calgary, Alberta. After two weeks in Kananaskis Country, Banff, Calgary, and other spots all over southern Alberta, we came away with the Good, the Bad, and the Ugly: The Good Alberta […]

A federal appeals court in Washington has struck down, for a second time, a rulemaking by the Federal Communications Commission to limit the size of the nation’s largest cable operators to 30% of the nation’s pay television marketplace, calling the rule “arbitrary and capricious.” The 30% rule, designed to keep no single company from controlling […]

Less than half of Americans surveyed by PC Magazine report they are very satisfied with the broadband speed delivered by their Internet service provider. PC Magazine released a comprehensive study this month on speed, provider satisfaction, and consumer opinions about the state of broadband in their community. The publisher sampled more than 17,000 participants, checking […]

Subscribe

Subscribe

“Comcast Corp.’s bid to buy Time Warner Cable Inc. may be the opening act for a yearlong festival of telecommunications deals that would alter Internet, phone and TV service for tens of millions of Americans.” — Bloomberg News, May 14, 2014

“Comcast Corp.’s bid to buy Time Warner Cable Inc. may be the opening act for a yearlong festival of telecommunications deals that would alter Internet, phone and TV service for tens of millions of Americans.” — Bloomberg News, May 14, 2014

Economists reviewing data found in publicly available corporate balance sheets soon found evidence that the “increased programming costs”-excuse for rate increases did not hold water. The less competition or number of choices available to consumers in the market unambiguously lead to higher prices. It has remained true since Consumers’ Union

Economists reviewing data found in publicly available corporate balance sheets soon found evidence that the “increased programming costs”-excuse for rate increases did not hold water. The less competition or number of choices available to consumers in the market unambiguously lead to higher prices. It has remained true since Consumers’ Union  When a cable operator pays such an outrageous price, the previous owner is reaping the financial rewards of his monopoly power. The acquiring company can only pay such a high price by assuming that his monopoly power will allow him to continue to increase prices. Monopoly power is being bought and sold and borrowed against. The new cable operator, who has paid for market power, may insist that the debt he has incurred to obtain it is a real cost on his books. That may be correct in the literal sense (he owes someone that money) but that does not make it right, or the abuse of market power legal.

When a cable operator pays such an outrageous price, the previous owner is reaping the financial rewards of his monopoly power. The acquiring company can only pay such a high price by assuming that his monopoly power will allow him to continue to increase prices. Monopoly power is being bought and sold and borrowed against. The new cable operator, who has paid for market power, may insist that the debt he has incurred to obtain it is a real cost on his books. That may be correct in the literal sense (he owes someone that money) but that does not make it right, or the abuse of market power legal.

As of May 1st, Frontier Communications has raised the price of its standalone DSL service $5 a month, primarily because its competitors have also raised prices.

As of May 1st, Frontier Communications has raised the price of its standalone DSL service $5 a month, primarily because its competitors have also raised prices. Despite the speed increases, cable competitors still made their presence known. Most cable companies sell faster service than Frontier offers and on the low-end, Time Warner Cable’s 2Mbps $15 broadband package, marketed to current DSL customers, was acknowledged to have an impact by Wilderotter, but not enough to bring a significant change in competitive intensity.

Despite the speed increases, cable competitors still made their presence known. Most cable companies sell faster service than Frontier offers and on the low-end, Time Warner Cable’s 2Mbps $15 broadband package, marketed to current DSL customers, was acknowledged to have an impact by Wilderotter, but not enough to bring a significant change in competitive intensity.