Subscribe

Subscribe AT&T is obviously a supporter of bringing its wireless customers closer together… in family plans, that is.

AT&T is obviously a supporter of bringing its wireless customers closer together… in family plans, that is.

The wireless carrier has adjusted its wireless data plans once again, this time in response to recent changes at Verizon and to better compete against T-Mobile — the carriers AT&T’s plans now most closely resemble.

Pricing wireless data has become a marketing art. Push people into too-small data plans and they will get stung with bill shock. Give them ample data at a high price and customers feel justified trying to use every last bit of it to get their money’s worth. So what is AT&T up to?

Light User/Budget Customers Squeezed

![]() If you keep your phone turned off except during special occasions, road trips, and landline service outages, AT&T has a plan for you. Actually, Verizon thought up most of these plans first — AT&T is now matching them as a consequence of the “competitive” market.

If you keep your phone turned off except during special occasions, road trips, and landline service outages, AT&T has a plan for you. Actually, Verizon thought up most of these plans first — AT&T is now matching them as a consequence of the “competitive” market.

AT&T’s $20 a month entry-level data plan offers a paltry 300MB of data, an amount so low it is likely to be consumed quickly just updating apps, reading web pages, and checking email. Although intended for light users, it is likely to expose customers to a nasty overlimit fee identical to the cost of the 300MB plan itself ($20 per 300MB). With embedded video advertising, bloated web pages, and growing-size apps that require regular upgrades, this kind of allowance is no longer tenable.

AT&T’s old 1GB and 3GB plans are also gone. Heads you may lose, tails AT&T usually wins. Customers on 1GB plans will now be herded into a 2GB plan that delivers twice the amount of data, for $5 more per month ($60 a year). That is a good value as far as wireless pricing is concerned, but only if you need twice the data. Customers with 3GB plans lose one-third of their allowance but get a $10 price break… unless they go over their limit and expose themselves to AT&T’s dastardly $15/GB overlimit fee. Then the savings evaporate.

The 2GB usage plan seems designed to keep you worried. Will you come perilously close to the overlimit fee again this month after watching those videos on the train? What about the 15 app updates that chewed through 300MB last week? With the average 4G iPhone customer in the United States using 1.8GB of mobile data each month during the summer of 2014, 2GB+ average usage is likely this year. Avoiding the overlimit fee will involve a costly leap into a more generous 5GB plan at a higher cost.

The New Normal: The 5GB Individual Plan/15GB Family Plan

It won’t be hard for AT&T to sell most customers on either a 5GB data plan if they have an individual account or a 15GB shared data plan for families.

The 5GB plan is $20 less than the 6GB plan it replaces. It’s presumably AT&T’s idea of a “sweet spot” for customers with a single line choosing between a $30 2GB plan that might not include enough data or a much more expensive 15GB plan — the next step up AT&T’s data plan range.

A close look at AT&T’s price chart shows the plan options and prices are designed to encourage individual line customers to migrate into a family plan. Here’s how AT&T does it:

Two AT&T customers with individual plans now pay $75 each for unlimited talk and text and 5GB of data. That adds up to $150 a month. But watch what happens when those customers take their vows as AT&T family plan customers. First, they each get a $10 break on the Plan Access charge ($15/mo each instead of $25). Second, there is more justification to spend $100 on a data plan that offers a more generous 15GB of data. Let’s look at the math:

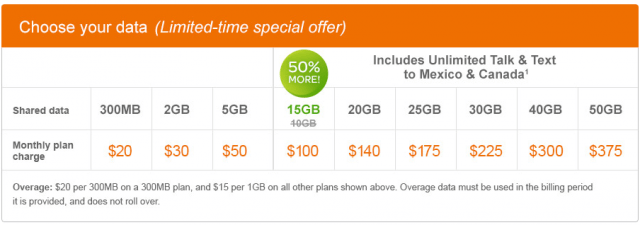

| Monthly Plans (now) | Monthly Plans (old) | Data (now) | Data (old) | Plan Access charge |

| $20 | $20 | 300MB | 300MB | $25 |

| $30 | $25/$40 | 2GB | 1GB/3GB | $25 |

| $50 | $70 | 5GB | 6GB | $25 |

| $100 | $100 | 15GB | 10GB | $15 |

| $140 | $150 | 20GB | 20GB | $15 |

Individual Plan (2 Lines)

2 x $25 Plan Access charge

2 x $50 5GB data plan

$150/month

Family Plan with 2 Lines

2 x $15 Plan Access charge

1 x $100 15GB data plan

$130/month — a $20 savings

Family plan customers pay $20 less and get an extra 5GB of mobile data. Customers choosing a data plan of 15GB or more also receive free unlimited calling and texting in Canada and Mexico.

Customers can be forgiven if they fall into the value trap – saving yourself into poverty. While AT&T’s recent price changes offer significant savings for certain customers, it is instructive to remember not so long ago AT&T charged $30 a month for unlimited mobile data, making the prospect of spending $100 for 15GB sanity-questionable. But that was then and this is now.

AT&T expects it will increase the amount of money it collects from each customer with the advent of these new plans, with the hope customers won’t remember back to the days where data usage was not monetized like a commodity.

That philosophy may still cost cable companies customers if a fiber competitor doesn’t have to compromise speed and performance and can afford to charge less.

That philosophy may still cost cable companies customers if a fiber competitor doesn’t have to compromise speed and performance and can afford to charge less.

When pressed for specifics, many wireless carriers eventually admit they have enough spectrum to handle today’s traffic demand, but will face overburdened and insufficient capacity tomorrow. But that is not what the evidence shows.

When pressed for specifics, many wireless carriers eventually admit they have enough spectrum to handle today’s traffic demand, but will face overburdened and insufficient capacity tomorrow. But that is not what the evidence shows. AT&T will soon have the highest activation fees in the wireless industry after an

AT&T will soon have the highest activation fees in the wireless industry after an