Subscribe

Subscribe Just weeks after FairPoint Communications and union workers settled a prolonged strike involving more than 1,700 workers that began last October,

Just weeks after FairPoint Communications and union workers settled a prolonged strike involving more than 1,700 workers that began last October,  FairPoint’s unionized workers returning to the job

FairPoint’s unionized workers returning to the job  Union leaders sense the company is already quietly getting the books in order for a sale.

Union leaders sense the company is already quietly getting the books in order for a sale.

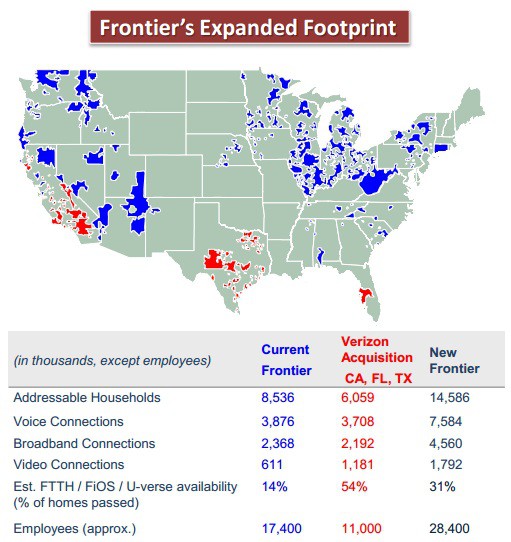

Dan McCarthy, Frontier’s president and chief operating officer, commented, “This transaction is an exciting opportunity for Frontier. We are well-positioned to maximize value for our shareholders and create a great experience for new customers. We have four FiOS markets today from our 2010 transaction with Verizon, and a high level of familiarity with the systems underlying these properties. We plan to flash-cut convert these properties to Frontier’s systems as we did in states including West Virginia and Connecticut.”

But Frontier’s “flash cut” conversions in West Virginia and Connecticut led to months of serious service and billing problems leading to two state-level investigations into Frontier’s performance. Problems are still ongoing in parts of Connecticut several months after Frontier transferred Connecticut territories from AT&T. Customers in West Virginia continue to criticize Frontier Communications for its underwhelming broadband performance.

But Frontier’s “flash cut” conversions in West Virginia and Connecticut led to months of serious service and billing problems leading to two state-level investigations into Frontier’s performance. Problems are still ongoing in parts of Connecticut several months after Frontier transferred Connecticut territories from AT&T. Customers in West Virginia continue to criticize Frontier Communications for its underwhelming broadband performance.

Saibus Research, a Wall Street analyst, said they were “stunned” Frontier was repeating the same mistake it made back in 2010 when it acquired other former GTE service areas from Verizon.

“We remembered that its $8.7 billion wireline purchase in 2010 did not work out so well for it,” wrote the analyst. “When we consider that Frontier’s share price declined by nearly 60% from 2010-2012 after the deal closed before recovering those losses since 2012, we were shocked that Frontier’s share price increased by 10.6% in response to its announcement that it was buying assets from Verizon. Frontier’s pro forma revenue has declined by 30% since 2009, its residential consumer base declined by 33%, its operating income declined by 34% and its dividend declined by 60% since then.”

“Albert Einstein said that insanity is doing the same thing over again and expecting a different result and we think that Frontier’s CEO Maggie Wilderotter has come down with a serious case of insanity for her willingness to buy whatever Verizon is selling,” said Saibus Research. “As such, we think income-oriented telecom investors should consider accumulating shares of Verizon, and selling or shorting Frontier.”

Frontier will accumulate billions in new debt to fund the transaction, bad news for legacy Frontier customers still served by the company’s copper wire networks. Frontier hoped to realize $500 million in cost reductions from its 2010 acquisition of Verizon territories in the Pacific Northwest, West Virginia, and several midwestern states. Instead of savings, it ended up spending millions to rehabilitate deteriorating landlines Verizon underinvested in for years. The new unsecured debt load will likely cut into available funds to upgrade older networks, particularly in the northeast and inside New York, Ohio and Pennsylvania.

Frontier will get marginal improvements in programming costs from the greater volume discounts its larger customer base qualifies to receive. But outside of Connecticut (Frontier U-verse) and Washington, Oregon, Indiana and South Carolina (Frontier FiOS), the rest of Frontier’s customers will continue to be offered Dish Network satellite service and various flavors of DSL.

If approved by regulators, the transaction will be finalized in 2016.

Cable One’s history as a former part of the Washington Post and its publishers — the Graham family — will come to an end next year as it is

Cable One’s history as a former part of the Washington Post and its publishers — the Graham family — will come to an end next year as it is